This article was originally published on the LightCastle Partners’ website

On the 6th of June 2024, Finance Minister Abul Hassan Mahmood Ali placed BDT 7,970 billion national budget for 2024-25 in parliament, which is only 4.6 percent bigger than that of the current fiscal year. The budget deficit for FY25 has been projected at 4.6% of the GDP, as opposed to 4.7% in the revised budget of FY24. ADP allocation has come down to 33.2% of total public expenditure, lower than the 34.3% in the revised FY24 budget.

The new proposed budget is intended to address the current macroeconomic challenges. However, certain policies or measures might result in contradictory outcomes, leading to reduced effectiveness of the instruments. This write-up will focus on the notable changes suggested in the budget and its short and long-term implications on businesses and the economy.

The economy is undergoing several headwinds, some particularly driven by external factors e.g. wars and global recessions, and others due to internal fault lines:

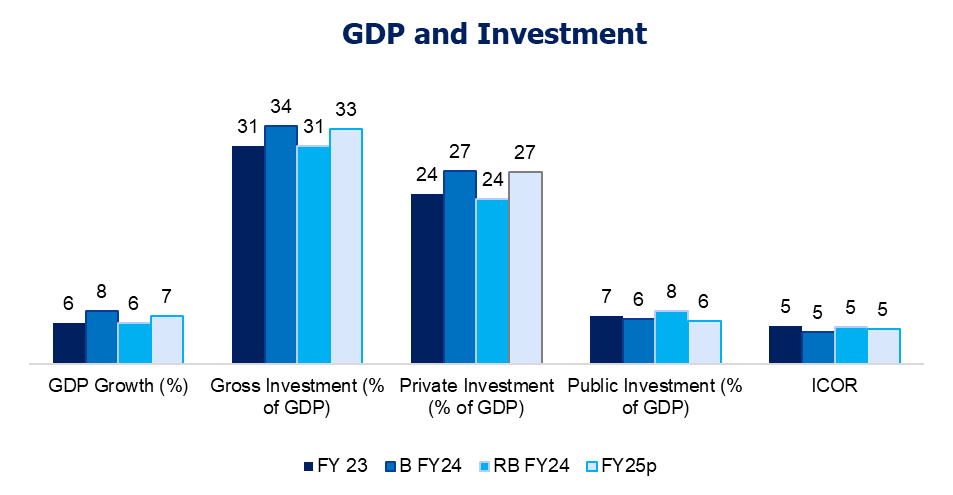

For FY25, the GDP growth target has been set at 6.8%, signaling a recovery from the provisional estimate of 5.8% for the Revised Budget FY24. The public investment-GDP ratio is projected to decline to 6.1% from 7.5% in FY24, representing a nominal decrease of BDT 367.6 Billion.

Conversely, the private investment-GDP ratio is expected to improve significantly, reaching 27.3% in FY25 compared to 23.5% in FY24. This increase implies an additional requirement of BDT 3,435.4 billion for private investment, reflecting a 28.9% nominal increase and indicating hopes for a substantial economic recovery.

However, the projection does not account for the impact of ongoing macroeconomic policy adjustments, such as contractionary monetary policy and a restrained fiscal stance. Additionally, the recent move to a deregulated interest rate regime and policy rate increase is expected to drive up interest rates. These policies could influence interest rates, inflation, and overall economic activity, potentially affecting growth and investment targets.

For the upcoming fiscal year, a total of BDT 7,970 billion is expected to cover the expenditure including BDT 5,069 billion in Operating Expenditure and BDT 2,814 billion in development expenditure. However, the budget showcases the possibility of a total revenue of BDT 5,454 billion including foreign grants of BDT 4.4 billion resulting in a fiscal deficit of BDT 2,516 billion.

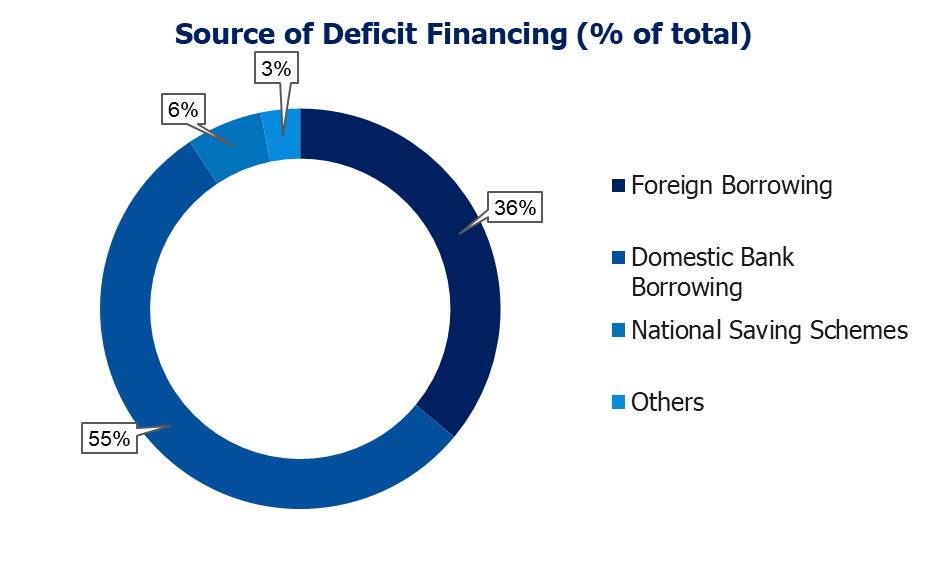

To mitigate the fiscal deficit, the government’s borrowing strategy involves a mix of foreign and domestic borrowing, each with specific advantages and drawbacks. While foreign borrowing provides substantial immediate funds, it increases future repayment obligations and exposes the economy to currency risks.

Increased foreign debt adds to the future repayment burden, which can lead to higher interest payments. This situation increases the vulnerability to exchange rate fluctuations, affecting economic stability and potentially leading to a depletion of FX reserves and further devaluation of the national currency.

On the other hand, while domestic borrowing will mobilize internal resources, potentially stimulating national investment, heavy borrowing from domestic banks may crowd out the private sector, making it more difficult and expensive for businesses to obtain credit. This competition for funds can lead to higher interest rates, reducing investment and slowing down economic growth.

The FY25 budget projections indicate a nuanced economic landscape characterized by reduced domestic financing dependency alongside increased bank borrowing, reflecting a potential strain on liquidity if not managed strategically.

The shift in strategy regarding National Savings Certificates (NSC) borrowing contrasts with previous net repayment predictions, signaling changes in government borrowing patterns. Furthermore, the heightened gross foreign aid requirement underscores a greater reliance on external financing sources, necessitating effective management of foreign debt obligations.

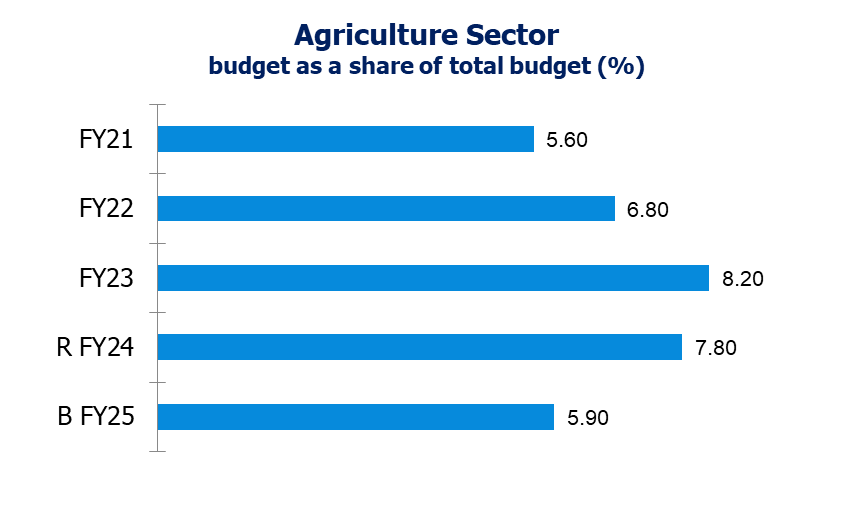

This year, the proposed budget reflects a balanced approach, emphasizing critical sectors like education, health, and public services while managing fiscal constraints. The public services sector and interest payments occupy the top two spots in terms of budget allocation. Conversely, the Local Government and Rural Development (LGRD) and agriculture sectors experienced notable declines in their budgets.

In the Budget FY25, the Agriculture sector has been allocated BDT 473.32 billion, marking a 15.5% decrease from the Revised Budget FY24. The expectation for FY25 is that the subsidy utilization will align with the proposed allocation, assuming the import prices of fertilizers continue their downward trend. However, considering the past trends of FY23 and FY24, there remains a possibility that the allocation may need to be revised to cover additional costs if fertilizer import prices do not decline as expected.

In the new budget, the Ministry of Agriculture’s funding increased to BDT 272,140 million from BDT 251,180 million in the current fiscal year. However, the subsidy for the agriculture sector decreased to BDT 172,610 million from BDT 175,330 million.

The 40% increase in the development budget for the Ministry of Agriculture (MoA) suggests a shift towards long-term agricultural development projects. This could lead to improvements in agricultural infrastructure, research, and technology adoption, which might enhance productivity and sustainability in the long run. However, the immediate benefits might not be felt by the farmers who are facing increased input costs.

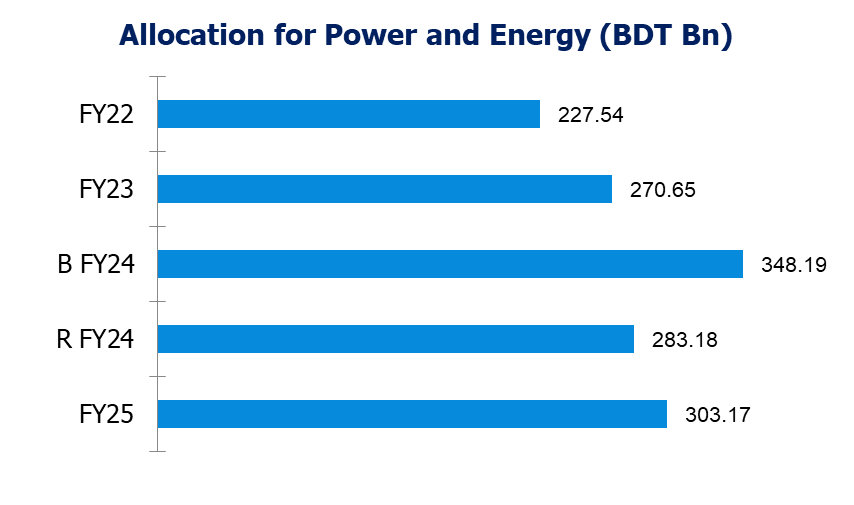

In the FY25 budget, the Power and Energy sector has been allocated BDT 303.17 billion, a 7% increase from the Revised FY24 budget. However, this allocation accounts for 3.8% of the total FY25 budget, a decrease from the 4.6% in the Revised FY24 budget. This reduction in the development budget is primarily due to an 11.54% reduction in project aid.

The reallocation of funds towards operational activities such as drilling new wells and expanding gas pipelines indicates a prioritization of immediate infrastructure needs over long-term development projects. A positive aspect is the higher allocation of the ADP budget towards developing transmission, with a reduced emphasis on generation.

For a nation burdened with high-capacity charge payments, this seems to be a move in the right direction. While this may address short-term demands, it could impact the sector’s capacity for innovation and growth in the future.

The government increased electricity prices in the country 3 times in 2023 by 15%. In March this year, electricity prices were again raised by BDT 0.34 to BDT 0.70 per unit. The increased rate has reduced the need for subsidies. In response to the IMF’s condition of phasing out subsidies to the power sector within the next 3 years, the government has drawn up a plan to increase the price of electricity on a quarterly basis for the next three years.

Moreover, the Bangladesh Petroleum Corporation (BPC) and Petrobangla have been allocated BDT 22.097 billion and BDT 22.534 billion respectively in the Annual Development Programme (ADP). Foreign aid comprises 56.5% and 49.1% of the total allocation for BPC and Petrobangla respectively.

However, the ADP allocation of the energy division has decreased by 12.7%, with the total number of projects decreasing from 11 to 9, albeit two gas mining projects from FY24 were completed last fiscal year. The Rooppur Nuclear Power Plant and the Matarbari Coal-fired power project account for 15.2% of total project aid in the Annual Development Program (ADP).

The significant reliance on foreign aid for projects undertaken by BPC and Petrobangla highlights the importance of maintaining strong diplomatic relations and securing external funding. However, fluctuations in foreign aid availability or changes in donor priorities could affect project implementation timelines and outcomes.

Under the Eighth Five-Year Plan, the goal was set to increase the education budget from 2% of GDP in FY19 to 3.5% by FY25. Despite this target, the allocation for education in FY25 stands at only 1.69% of GDP. This places Bangladesh at the lower end of educational investment, with its average expenditure on education as a percentage of GDP from 2016 to 2023 being the third lowest among 38 Least Developed Countries (LDCs).

In contrast, at least 33 of these countries consistently allocated 2% or more of their GDP to education during the same period. Additionally, the FY25 budget imposes a 15% corporate tax on private academic institutions, effectively increasing the financial burden on students and potentially hindering access to higher education.

This is particularly concerning given the urgent need to enhance skills in the employment sector, within the context of the nation’s graduation from LDC status. Despite these challenges, it’s noteworthy that the share of the education budget relative to the total budget and GDP has seen an increase from 10.44% in the revised FY24 budget to 11.88% in the FY25 proposal.

The total budget allocation for health has increased by 9%, from BDT 380,500 million in FY24 to BDT 414,080 million in FY25. However, health spending per person only saw a marginal increase of BDT 186, from BDT 2,227 in 2023 to BDT 2,413 in 2024.

The 9% increase in the total health budget and the marginal per capita spending increase suggest that while there are improvements, they may not be substantial enough to address the underlying healthcare challenges. The modest increase in per capita spending (BDT 186) may not significantly impact overall healthcare quality and accessibility.

The combination of low GDP expenditure, minimal per capita spending, and targeted budget cuts suggests systemic challenges in healthcare funding in the country. The WHO recommends maintaining a doctor-patient ratio of 1:1000. According to the last report by the WHO, Bangladesh has just 5.26 doctors per 10,000 patients, significantly below the recommended ratio. Better governance within the health system should also be prioritized since it increases resource utilization.

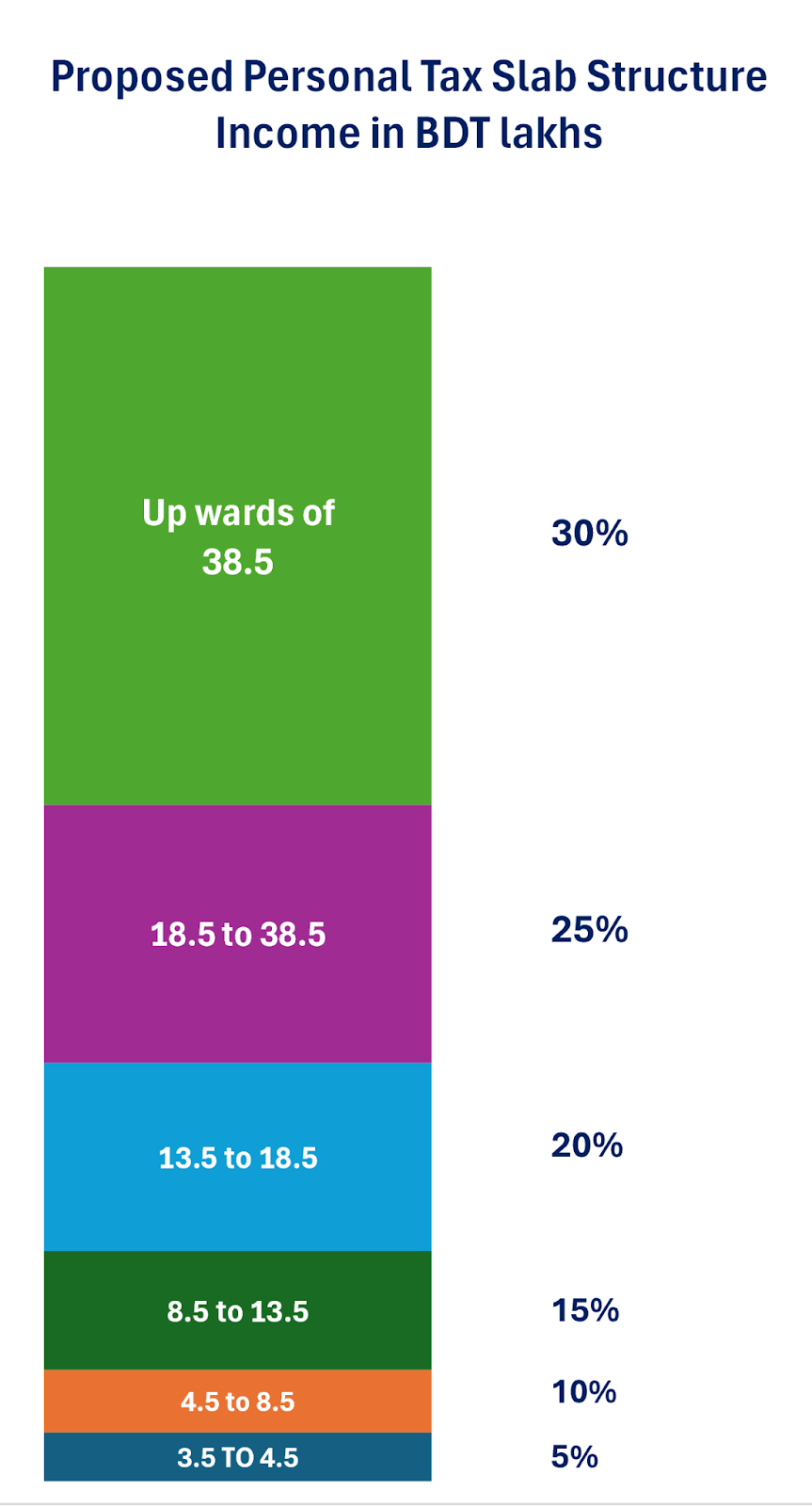

The minimum tax-free limit remains unchanged from last year. Some argue that this limit should have been raised to increase the disposable income of lower-income individuals, especially considering high inflation. However, the new tax structure does provide some relief for upper-income individuals by raising the 10% tax slab threshold from BDT 750,000 to BDT 850,000.

The budget also focuses on wealth redistribution by increasing the highest tax rate for top earners from 25% to 30%. Hence, the revised structure is expected to boost savings, particularly in rebate-eligible securities from higher-income individuals. Within the deregulated interest rate regime, this change might help the government meet its target financing through National Savings Certificates.

Overall, the new tax regime aims to support the economy during a slowdown. However, given our current macroeconomic scenario, a more pro-poor policy could have involved raising the minimum tax threshold and setting the highest tax slab at a lower amount than BDT 3.85 million.

According to data from the National Board of Revenue (NBR), the number of Taxpayers’ Identification Number (TIN) holders reached 9.72 million in the individual taxpayer category during the last year. The total number has to increase to bring about substantial growth in total tax revenue.

The FY2025 Budget has implemented several adjustments to the country’s tariff structure, each designed with specific impacts on the economy in mind. A summary of these key changes includes:

The revisions to VAT and supplementary duties outlined in the FY25 budget reflect a strategic approach to balance economic development with health and social considerations. Increased duty on telecommunication services is expected to pass on to the consumers, hindering prospects of digital inclusion, internet penetration, and access to information, particularly for the rural low income population.

The FY2024-25 budget’s proposals to support domestic industries in Bangladesh are strategically aimed at fostering economic self-sufficiency and boosting local production. By adjusting import duties and VAT, these measures protect indigenous producers, such as those in the agriculture sector, and promote the competitiveness of domestic manufacturers in textiles and heavy industry.

For instance, the imposition of duties on imported cashew nuts protects local farmers. Reducing import duties on manufacturing inputs like polypropylene yarn encourages the growth of industries like carpet manufacturing, supporting domestic production capabilities and reducing import dependency.

However, these measures might also increase production costs if domestic alternatives are less cost-effective, potentially leading to higher consumer prices and affecting the global competitiveness of Bangladeshi products. The removal of VAT on aircraft engine parts is a significant step to support the aviation sector against international competition, potentially lowering operational costs.

The budget has introduced a “no questions asked” provision allowing individuals to invest undisclosed money into the economy by paying a 15% tax on the amount. This initiative aims to bring money back into circulation. Since independence, governments have used similar measures, legalizing about BDT 470,000 million.

Notably, about BDT 330,000 million was legalized during the ruling Awami League’s terms since 2009. During the pandemic in the fiscal year 2020-2021, BDT 206,000 million was legalized by 11,859 people, largely because international travel had halted and the hundi system had slowed down, making it difficult to move money out of the country.

However, without such circumstances now, the effectiveness of this measure is questionable, especially since the highest tax rate for legal income is 30%. This creates an incentive for individuals to keep their earnings undisclosed, avoid the 30% tax, and later bring the money back into circulation at a reduced rate of 15%. The practical impact of this provision remains uncertain.

For the poor, a crucial source of support is the government’s social safety net (SSN) programs. The overall SSN budget increased slightly as a percentage of the total budget, from 17% in the revised FY 2023-24 budget to 17.1% in the proposed FY 2024-25 budget. Similarly, the SSN budget as a percentage of GDP rose from 2.40% to 2.43%. However, pensions for retired government employees and their families, interest from savings certificates, and agricultural subsidies account for 46% of the total SSN allocation. Excluding these items, the portion of allocation drops significantly to 1.32% of GDP.

This exclusion underscores the significant impact these specific allocations have on inflating the apparent size of the SSN budget. Allocation for social safety nets has increased by only 12%, whereas allocation for pension has increased by 36%. Under the Open Market System (OMS) program, the government sells rice and flour at low prices for the low-income population. The program is especially crucial under the current circumstances, with food inflation hitting 10.22% (BBS, 2024) in April. However, the allocation to the OMS program saw a 64% decrease, down BDT 20,040 million from the revised FY24 budget of BDT 54,910 million.

The reallocation of funds from less impactful allocations to targeted social protection programs could result in a more efficient and equitable distribution of resources.

The corporate tax rate has been revised and increased by 2.5%, albeit subject to conditions. A push towards digital payments has been institutionalized. Corporations that exclusively use bank transfers to transact any income, receipts, expenses, and investments exceeding BDT 500,000 per transaction and BDT 3.6 million annually will be able to enjoy the 25% tax rate, while 27.5% will be applicable for the rest.

While a push towards digital payments is commendable, there is doubt regarding the proportion of mid-sized corporations being able to reap the benefits of the incentive. Under such circumstances, the effective tax rate will increase, discouraging further investment and expansion. Amidst the economic slowdown and higher tax regime, corporations are expected to report lower profits, casting doubt on the government’s ability to meet its revenue collection target from corporate taxes.

The situation could render worse outcomes for SMEs. From a broader economic perspective, higher interest rates and increased domestic borrowing could restrict financing for the private sector, particularly for SMEs that already struggle with financial credibility and collateral.

This is especially concerning during an economic slowdown, as large projects and investments that create jobs are likely to decrease. Within a higher tax regime and constrained overall demand, the viability of SMEs comes into question. Without access to financing, these companies may fail, affecting their workers and leading to tough economic conditions for some lower-income families.

As part of new fiscal measures, investors and developers in private economic zones (EZs) and hi-tech parks will face significant changes from the next fiscal year. The government is phasing out the 10-year tax waiver on their incomes, which has been a major incentive for investment. Additionally, the previous zero-duty benefit on the import of capital machinery, components, and construction materials has been revoked. Starting in FY25, firms operating within these industrial enclaves will be subject to a 1% customs duty. These changes are likely to disincentivize investments and could negatively affect foreign direct investment (FDI) inflows, which are vital for the country’s economic progress at this crucial time.

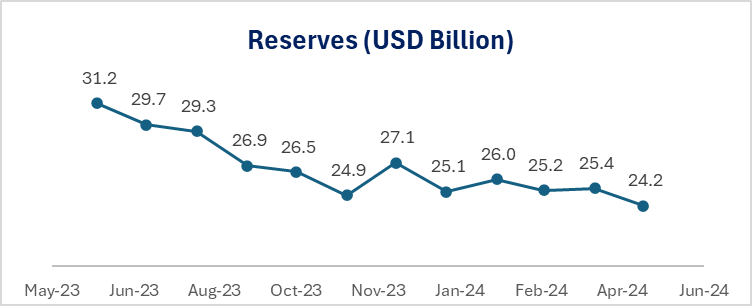

The foreign currency reserves of Bangladesh have been on a downward trend, declining by 24.7% over the last 12 months. This has led to a sharp devaluation of the BDT against the USD, making essential imports like energy more expensive and driving domestic inflation. To address these issues, the government has implemented measures such as import restrictions and introduced a market-based exchange rate, which is expected to stabilize the currency.

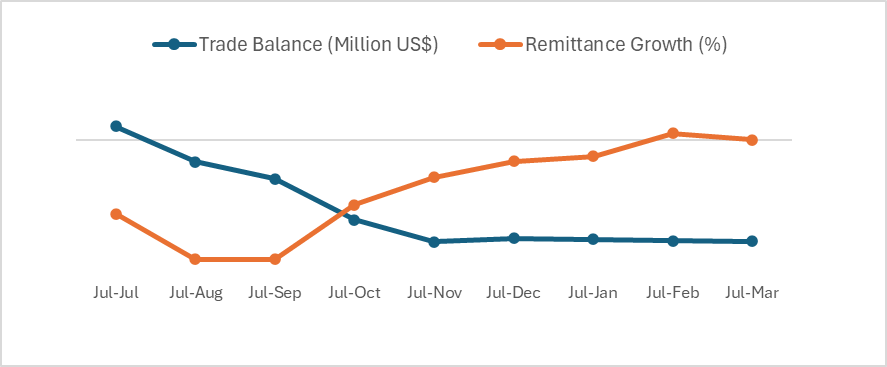

Although the trade balance appears to be stabilizing, that has been mostly driven by restrictions in opening LCs to restrict imports. While effective in the short term, it cannot be considered a sustainable strategy to improve balance of trade. The FY2024-25 budget sets a reserve target of USD 32.3 billion. Although achieving an increase of USD 8.1 billion within a year seems optimistic, there are signs of hope. Remittance flows have increased over the past six months.

With a higher exchange rate for the dollar, further increases in inflows are anticipated, as it incentivizes transfers through formal banking channels. Depreciation of the currency also increases the country’s export competitiveness. The ideal scenario would be an improved balance of payments and sustained growth of remittance inflows, gradually replenishing the foreign currency reserves.

The FY2024-25 budget signals a contextually appropriate contractionary policy, but its implementation will be crucial. Key issues to watch include how the economy balances the slowdown while ensuring employment, especially for low-income families. A significant factor will be the government’s ability to collect the budgeted direct tax revenue.

The target for revenue collection decreased by BDT 224,000 million in the revised budget of FY2023-24. A similar shortfall could necessitate further financing from domestic or foreign sources, both of which carry undesirable short-term and long-term consequences for the macroeconomy. The ADP implementation was also revised and decreased by BDT 180,000 million in the last year.

Revenue composition for the FY25 indicates 33.8% coming from VAT sources. High reliance on VAT for revenue might contribute to further inflation since it impacts consumer prices. If our currency depreciates further, import costs will keep rising. Since we depend on imports for a lot of essential inputs, rising costs will make containing inflation increasingly difficult. Currency depreciation will also increase interest payments for foreign loans. Remittance flows and exports must grow sustainably in order to avoid such a scenario.

Several issues remain unresolved, such as the inclusion of government employees’ pensions and agricultural subsidies under the SSN program, the outdated methods of government revenue collection, and the lack of significant investments in long-term national value creation like education, skills development, and healthcare. Additionally, the monetary policy should be revisited during FY25 to ensure its alignment with the proposed fiscal policies. Overall, there is doubt that the reduced target inflation rate of 6.5% will be achieved, the inherent objective of this year’s budget.

This article was authored by Priyo Pranto, Business Consultant, and Dipa Sultana, Senior Business Consultant and Project Manager at LightCastle Partners. Advisory support was provided by Zahedul Amin, Director at LightCastle Partners. For further clarifications, contact here: info@lightcastlebd.com

Gain perspectives of the emerging sectors of Bangladesh

InsightsContact us for a comprehensive understanding of the investment landscape in Bangladesh