The Ready-Made Garments (RMG) sector continues to serve as the backbone of Bangladesh’s export-oriented industrialization, maintaining its dominance in the country’s economic structure. As of 2025, the sector recorded USD 39.34 billion in export earnings, with knitwear accounting for USD 21.16 billion and woven garments for USD 18.19 billion. Early 2025 data indicate a recovery in Foreign Direct Investment (FDI), particularly in high-tech textile segments and export processing zones. The industry is backed by the highest number of green garment factories globally, with over 230 LEED-certified units, supported by government initiatives promoting sustainable manufacturing and environmental compliance.

The sector remains heavily concentrated in key markets, with the United States and European Union dominating exports. During October-December of FY24, the top nine export destinations accounted for 67.56% of total RMG exports, highlighting continued market concentration risks. Knitwear continues to lead the export basket, contributing to a larger share than woven garments, indicating relatively stronger domestic backward linkages.

Despite its scale, the industry remains dependent on imported raw materials. In Q2 FY2024, imports of raw materials, including cotton, yarn, and fabrics, stood at USD 3.37 billion, accounting for 28.65% of total RMG export value, reflecting limited backward integration, particularly in woven and synthetic segments.

The sector also faces increasing structural and external challenges. These include rising production costs due to energy price volatility, exchange rate depreciation, and global inflationary pressures, alongside declining demand in major markets. Additionally, Bangladesh’s upcoming LDC graduation in 2026 is expected to impact competitiveness through the gradual loss of trade preferences, requiring significant improvements in productivity and compliance standards.

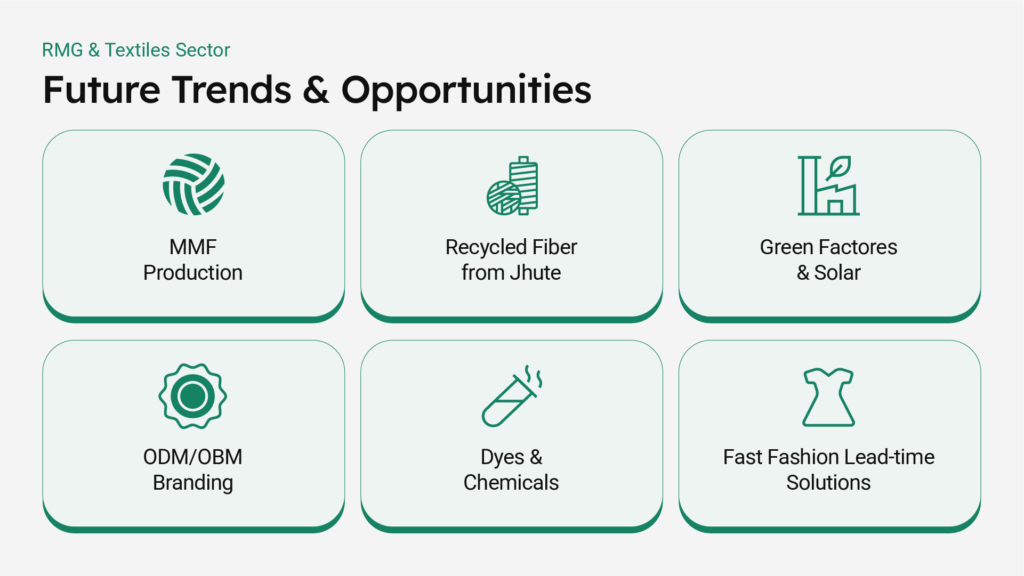

At the same time, the industry is undergoing a transition toward higher value addition and sustainability. There is growing emphasis on green manufacturing, compliance with international standards, and diversification into man-made fibre (MMF) products, which dominate global textile demand. Overall, as of 2024–2025, Bangladesh’s RMG and textile sector remains a resilient, export-driven industry, balancing strong global positioning with the need for diversification, technological upgrading, and policy adaptation to sustain long-term growth.

Key Factors Driving the RMG and Textiles Industry

Bangladesh’s RMG sector has grown due to several pivotal drivers. These factors encompass the country’s extensive history of textile production, a cost-effective labor force, export facilitation measures, and trade agreements such as the Generalized System of Preferences (GSP).

Apparel continues to dominate Bangladesh’s export landscape, remaining the country’s largest export-earning sector and a key driver of foreign exchange earnings. Europe remains the largest export destination for Bangladesh’s RMG exports, followed by key markets such as the United States and the United Kingdom.

Bangladesh’s RMG sector has continued to demonstrate resilience, recording a 6.34% growth in export earnings during the January–March period of FY2025–26, despite ongoing global and domestic challenges. At the same time, exports to the United States have shown strong growth, with RMG exports reaching USD 2.12 billion during July–September 2025, up from USD 1.87 billion in the same period of the previous year, indicating strengthening demand in key markets.

To ensure sustained export growth, diversification of the product basket remains critical. Bangladesh’s current export portfolio is largely concentrated in basic apparel, while expanding into man-made fiber (MMF)-based apparel and higher-value products presents significant opportunities to capture evolving global demand.

Moreover, the shift toward circular fashion and sustainability-driven production is becoming a key determinant of export competitiveness. Increasing regulatory requirements in major markets, particularly in Europe, related to traceability, recycling, and environmental compliance, are reshaping sourcing decisions and market access. At the same time, post-LDC graduation dynamics may introduce tariffs of up to 11.8% in the EU market if GSP+ conditions are not met, further emphasizing the need for compliance-driven competitiveness.

Overall, Bangladesh’s RMG and textile sector holds strong export potential, supported by established global market linkages, rising demand in key markets, and emerging opportunities in sustainability-driven apparel. Future growth will depend on product diversification, technological upgrading, and alignment with evolving global trade and regulatory standards.

Manufacturers: The largest industry in the country is represented by the Ha-Meem Group, which operates 26 garment factories across Bangladesh. Another prominent garment manufacturing company is Beximco, which commenced operations in 1997. BAL is a 100% export-oriented clothing manufacturer specializing in the production of woven material clothing. DBL Group is a leading multi-faceted garment and textile manufacturing company with a workforce of approximately 35,000 employees. Other significant players include the Faki Group, Square Fashions LTD, and the Epyllion Group, among others.

Buyers: Currently, there are more than 100 international brands that source apparel from Bangladesh. Some of the top clothing brands that engage in sourcing from Bangladesh include Marks & Spencer, Calvin Klein, Lee, H&M, Supreme, American Eagle, Zara, Gap, Tommy Hilfiger, and many others.

Additionally, Bangladesh holds untapped potential in leveraging its approximately 440,000 tonnes of annual textile waste (jhut), which can be converted into recycled raw materials for higher-value apparel production. Strengthening recycling and circular supply chains can reduce import dependency while expanding export opportunities in a sustainable fashion.

The garment industry in Bangladesh faces a range of difficulties. These encompass the escalation of labor costs, heightened competition from other cost-effective nations, and the imperative to improve working conditions and environmental sustainability. Additionally, the sector is contending with the ramifications of technological progress and the automation revolution, which are fundamentally reshaping the worldwide garment industry.

Gain perspectives of the emerging sectors of Bangladesh

InsightsContact us for a comprehensive understanding of the investment landscape in Bangladesh