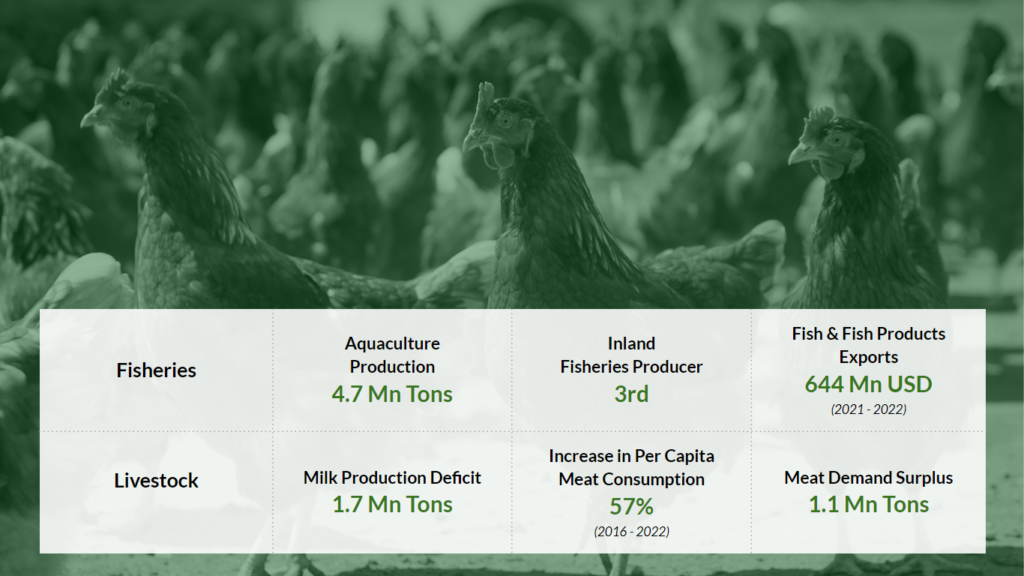

The livestock & fisheries sector, a vital component of Bangladesh’s economy, contributed 4.5% to the GDP in FY 21-22. Growth of the industry has been led by the rise in disposable incomes and economic prosperity. This economic upturn has led to a diversification in dietary habits, resulting in increased consumption of animal-based proteins like fish, poultry, beef and dairy products. Between 2016 and 2022, consumption of meat, saw a notable 57% surge, while milk consumption experienced a 25% rise within the same time period.

In FY 2021-22, Bangladesh’s fisheries sector continued its significant contribution to the economy, with aquaculture production of 4.7 million metric tons Bangladesh ranks 3rd globally in inland water capture, cage culture, and pen culture production. Key species like carp, pangasius, and tilapia are central to freshwater fish production. Shrimp farming also thrives, with 261 thousand metric tons produced in 2021-22. As consumer purchasing power grows, there’s a shift toward higher-value species and processed fish products, especially in urban areas. Production is geographically dispersed, with Mymensingh, Jessore, and Comilla leading. The sector has room for improvement in genetics, disease control, feed quality, post-harvest practices, cold chain development, and supply chain optimization, promising sustainability and competitiveness.

The poultry industry in Bangladesh has four main production systems: traditional rural, semi-scavenging, commercial, and contract farming. Until 2000, commercial poultry farms relied on imported Parent Stock (PS), but local companies started their operations, boosting poultry production. Efficiency has improved with the introduction of high-yield breeds. Competition in commercial poultry farming has increased, shifting from ‘low volume and high margin’ to ‘high volume and low margin’ investments due to national competitive advantages. Most poultry farms operate at a household level, limiting expansion and technology adoption, given Bangladesh’s developing status. Approximately 37% of the total meat produced in Bangladesh is poultry.

The cattle industry in Bangladesh has seen significant growth in recent years, even amidst challenges posed by the Covid-19 pandemic. Other than the macro economic development, one of the key driving forces behind the robust growth in the cattle sector has been the decline in illegal cattle imports from India. This shift has catalyzed the development of a strong indigenous dairy sector. Additionally, farmers have become more knowledgeable about animal husbandry and genetics, opting for high-yielding exotic and cross-bred cattle breeds over the less productive local varieties.

Key Factors Driving the Livestock & Fisheries Industry

Growing Demand Fueled by Rising Per Capita Income leads to higher demand for products as people shift to protein-rich diets.

The growing hotel, restaurant, and catering sector creates consistently rising demand for livestock & fisheries products.

Establishment of modern storage and processing facilities reduce losses, maintain product quality, and enable value addition.

Improved transportation infrastructure connects rural areas to urban markets, improving market access and reducing cost of transportation.

Government initiatives to promote high-yield, disease-resistant breeds, enhancing productivity.

Adoption of modern farming technologies boosts productivity. Livestock population increased by 2.4% in the last 4 years, while meat production increased by 3.8%, indicating a rise in productivity.

Exports provide an additional market, especially for aquaculture products, incentivizing quality production.

Export Potential

Bangladesh exported 644 Million USD worth of Fish & Fish products in FY 2021-22, of which, 70% came from frozen shrimp exports. Major export destinations are the EU and the USA. The frozen fish sector currently enjoys 7-10% cash incentive on shrimp exports and 2-5% on other fish exports.

The export market of the livestock sector is not very well developed, since Bangladesh very recently moved into production surplus, after meeting domestic demand. However, the development of the post-processing industry, and the rise in productivity due to mechanization, development of deep sea ports exhibits the export potential of the sector. The total export of Live Animals, Meat, Dairy, and Eggs amounted to USD 1.08 million in the FY 2021-22.

Market Dynamics

The livestock sector covers cattle (milking and fattening) and poultry (broiler and layer) farming, while the fisheries sector is composed of Inland Capture, Culture, and Marine Fisheries.

Bangladesh has over 125 aqua processing facilities, primarily situated in port cities like Khulna and Chittagong. The level of fish processing is relatively modest, with a preference for fresh sales in wet markets. However, there’s an anticipated rise in retail sales of processed fish, paralleling the improvement in overall welfare. In contrast, shrimp processing is notably more extensive, involving freezing before exportation. In pursuit of higher-value markets in Europe, processors have made substantial investments in advanced processing techniques, extending beyond IQF and block freezing to incorporate Ready-To-Cook lines. Notably, Alpha Seafood invested USD 3.5 million in 2019, followed by Primus Seafood with USD 2.4 million, and ACI-Godrej with USD 1.8 million.

Private sector initiatives, coupled with government policy support, have played a pivotal role in fostering competition in commercial poultry farming. Initially, the sector attracted investments characterized by ‘low volume and high margin‘ strategies. However, the competitive landscape has undergone significant changes, with the industry now experiencing heightened competition due to national competitive advantages. This shift has created an environment of ‘high volume and low margin‘ investments, reflecting the industry’s adaptability to evolving market dynamics. However, most poultry farms in Bangladesh still operate at a household level, limiting their ability to expand and acquire advanced technological equipment.

Commercial cattle farming activities are primarily concentrated in the North-Western districts of Bangladesh. The majority, approximately 93%, of beef cattle are raised by smallholders who typically possess 1 to 5 cows. These smallholders are often engaged in dairy farming, either selling their older dairy cows or raising a single bull for religious slaughter. A smaller segment, around 6%, consists of medium-sized farmers who own 10 to 20 cows, while only 1% are considered large farmers with holdings of more than 100 cows. Among these, only the large and very large farms provide commercial concentrate feed to their beef cattle, representing a minor fraction of the overall beef cattle industry in Bangladesh.

The larger commercial players of the industry are vertically integrated, with players like Paragon, Aftab, Kazi, producing their own feed. Few players are also integrated at the forward market, for example, Gemini through their retail superstore, Meena Bazar.

Challenges, Trends and Opportunities

Challenges

Lack of Mechanization: One of the prominent challenges in the sector is the limited mechanization of farming practices. Traditional, labor-intensive methods prevail in many areas, leading to inefficiencies, higher labor costs, and lower overall productivity. Mechanization, such as the use of modern farming equipment and technology, could significantly enhance production and reduce manual labor.

Limited Adoption of Contract Farming: The absence of widespread adoption of contract farming arrangements in Bangladesh poses challenges for both farmers and investors. Contract farming can provide stability and predictability in the supply chain, but its limited implementation means that producers often face market uncertainties and difficulties in accessing financing.

Insufficient Technical Capacity: A lack of technical expertise and knowledge among farmers is another pressing issue. Many small-scale farmers may not have access to modern farming techniques, proper training, or information about best practices. Enhancing technical capacity through training programs and knowledge dissemination is crucial for improving productivity.

Import Dependency of Inputs: The livestock sector is import dependent in terms of feed. 90% of the soybean (raw material for feed production) has to be imported, exposing the sector to exchange rate risks and supply chain crises

Price Volatility: Depending on the global feed market, market prices of meat and eggs fluctuate at the consumers’ end

Value Chain Inefficiency: Currently, the livestock value chain is complex, consisting of high number of intermediaries, leading to inefficiencies and unequal margin distribution among the actors

Opportunities

Vannamei Shrimp: The approval of higher-yield vannamei shrimp varieties in Bangladesh marks a significant development in the country’s aquaculture sector. These new shrimp strains promise increased productivity, offering the potential for higher yields per hectare of shrimp farms. This advancement aligns with the sector’s ongoing efforts to meet growing global demand for shrimp and enhance the competitiveness of Bangladesh’s shrimp industry.

Underdeveloped post-harvest processing: The underdeveloped post-harvest processing sector in livestock and fisheries presents an attractive investment opportunity. Outdated methods and inadequate infrastructure result in substantial losses. Modern processing facilities and technology investments can reduce losses and increase product value, aligning with rising demand for processed goods and fostering sector growth and profitability.

Dairy Products: The consumption of milk and dairy products in Bangladesh has been on a robust growth trajectory, Despite efforts to expand production capacity, demand consistently outpaces supply, creating a domestic market gap. With per-capita consumption of milk and dairy products in the country below the WHO’s recommended level, there exists substantial investment potential in the sector.

Processed Meat: Meat consumption in Bangladesh has steadily risen, driven by the growth of poultry farming and the expanding restaurant and hotel industry. The processed food market, as reported by Euromonitor International, is anticipated to maintain strong growth at over 13% annually until 2023. Furthermore, the global halal meat market offers an additional avenue for the Bangladeshi industry to explore.

Frozen and Ready-to-Cook Food: The frozen and ready-to-cook food segment in Bangladesh has seen rapid expansion, driven by growing urbanization, increase of the MAC population and shifts in dietary preferences. The market is projected to reach approximately USD 355 million by 2024, as indicated by Financial Planning research.