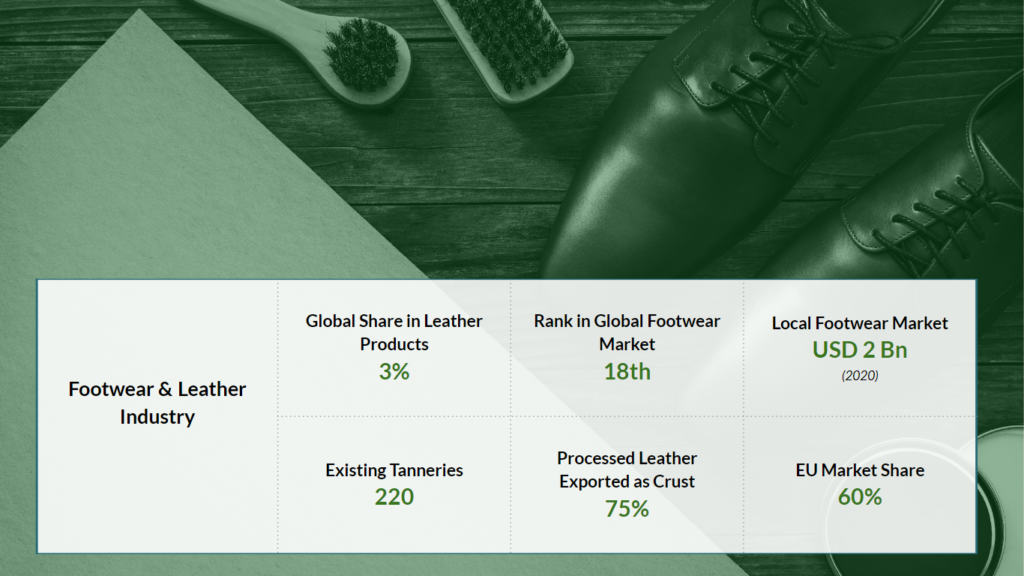

The leather and leather goods industry in Bangladesh, one of the country’s oldest sectors, has been a significant contributor to the national economy for many years. This industry serves both domestic and international markets ranking second in export earnings. Despite its considerable potential, nearly 40% of the local demand is met through imports. Bangladesh ranks 18th in the global footwear market. In the global leather and leather products market, Bangladesh holds a 3% share, and it represents 10% of the worldwide leather market. In 2020, the local footwear market was valued at approximately USD 2 Billion, with an annual production of 378 million shoes, while the local market demand is around 200-250 million pairs annually.

This industry encompasses four main product segments: tannery output (hides and skins), finished leather, leather goods, and leather footwear. The country produces various products such as bags, purses, luggage, belts, wallets, jackets, and footwear, with footwear being a significant product category in Bangladesh. The industry consists of around 3,500 small-scale, 90 medium-scale, and 15 large-scale manufacturers, along with 220 tanneries, as reported by the Leather Goods Association. The footwear and footwear components sector plays a substantial role in the leather industry, with 2,500 footwear units and 90 large firms. The leather industry in Bangladesh is primarily concentrated in Hazaribagh District near Dhaka, followed by Bhariab and Chattogram.

Bangladesh possesses a substantial quantity of locally available raw materials, including a significant cattle stock (around 1.8% of the global total) and goat stock (3.7% of the total). The country has the potential to supply a substantial volume of raw leather, approximately 350 million square feet annually. However, only a small portion of raw leather is processed into finished leather, and the majority (75%) of locally processed leather is exported as crust without adding significant value. Interestingly, finished leather can command a price up to 60% higher than crust leather. This situation has led Bangladeshi exporters to import wet-blue materials, resulting in a 40% to 50% increase in production costs.

The BCI score of +2.42 primarily arises from a consistent evaluation of the sector’s past performance and a positive outlook for future recovery. Even though the sector has encountered difficulties related to decreased global consumer demand, rising import expenses, and a shrinking profit margin, it has managed to achieve growth in both volume and value, driven by strong domestic demand.

Key Factors Driving the Footwear and Leather Industry

Increasing income levels coupled with a substantial domestic market: The expanding middle-class demographic in Bangladesh has led to higher consumption of leather products, encompassing items like footwear, bags, and accessories. This surge in demand has propelled the growth of the local leather industry.

Highly cost-effective labor force: This labor-intensive sector efficiently employs approximately 200,000 individuals directly and another 850,000 indirectly, as reported by the Asian Development Bank (ADB). The leather industry serves as a notable example of its ability to effectively absorb unskilled labor. Workers typically start as unskilled trainees and progressively advance to become semi-skilled and skilled workers through on-the-job training.

Beneficial duty-free market access: Bangladesh enjoys duty and quota-free access to developed countries, including the EU, UK, Japan, Canada, Russia, and Australia, under programs such as the Generalized System of Preferences. In contrast, leather products from China, a significant competitor, face additional duties when entering these markets, highlighting the industry’s potential for export competitiveness. However, it’s important to note that the country may lose these GSP privileges once it graduates from its status as a Least Developed Country (LDC).

Abundant supply of raw materials: The sector’s greatest strength lies in its abundant supply of raw materials. Bangladesh consistently sources hides and skins from the local cattle population and other animals, ensuring a steady input stream for the leather industry. Notably, approximately 50% of the annual rawhide collection occurs during Eid-ul-Azha, the second-largest religious festival, which is subsequently processed to provide leather.

Government incentives for the industry: The Bangladeshi government has extended various forms of support, including financial incentives and policy reforms like the Leather and Leather Goods Development Policy 2019, aimed at promoting growth and enhancing compliance within the leather sector.

Export Potential

Approximately 85% of Bangladesh’s leather and leather products find their way to international markets, primarily in the forms of crust leather, wet-blue leather, finished leather, leather clothing, and footwear. The majority of these exports are destined for countries like the European Union (EU), the United States, Australia, Japan, Singapore, South Korea, and others. When it comes to footwear exports, the European Union (EU) leads the way, capturing a majority share of 60%, followed by Japan with a 30% share. In the broader category of leather and leather goods, the EU claims a significant portion, accounting for 33%, while Japan holds approximately 8% of the market share. Furthermore, there is a target by the government to increase leather export earnings from USD 1 billion to USD 10-12 billion by 2030.

If the abundant quantity of locally available raw materials can be converted into finished leather products then it is likely to attain higher export value and capture more markets.

Market Dynamics

Once the local demand is fulfilled, any excess footwear is exported to international markets. As a result, renowned global brands like ABC Mart, Adidas, Aldo, Esprit, Hugo Boss, H&M, Kate Spade, K-Mart, Michael Kors, Marks & Spencer, Nike, Steve Madden, Sears, Timberland, and many others rely on Bangladesh as their source for leather goods and footwear. Moreover, Apex Footwear presently stands as one of the largest shoe manufacturers in South Asia, contributing to approximately 15% of Bangladesh’s exports of leather footwear as of 2022.

Government Support & Policy Incentives

The Leather and Leather Products Development Policy 2019, introduced in August 2019, encompasses a range of incentives aimed at enhancing the sector’s export earnings. It is recognized as a high-priority industry in both the current Export Policy and the National Industry Policy of 2016. The government is establishing three industrial estates dedicated to leather and tannery industries in Rajshahi, Savar, and Chattogram.

The following incentives are provided to the sector:

Reduced Corporate Income Tax (CIT) for a duration of 5 to 10 years, depending on the location.

Import duty exemption on capital machinery.

Exemption from regulatory/supplemental duties for footwear producers using specific materials like tubes, pipes, plastic, PVC screens, and textile/knitted fabric.

50% tax exemption for income generated from exports.

No imposition of Value Added Tax (VAT) on exported goods.

Provision of bonded warehousing facilities for substantial material imports.

A 15% cash incentive on the export value of leather goods and footwear, with an additional 5% for crust leather from the Savar Estate.

In addition, the Leather and Leather Goods Development Policy 2019 seeks to enhance compliance, waste management, the capacity of Common Effluent Treatment Plants (CETPs), and factory conditions. However, challenges in implementation have been encountered.

Investment Challenges and Mitigation Strategies

Some of the challenges include:

The absence of a comprehensive policy framework, including a lack of a long-term strategy for Common Facility Centers (CFCs), SME cluster development, and the promotion of Bangladesh leather products.

Insufficient development of backward linkage industries for chemicals and accessories, along with issues related to the subpar quality of products.

The stringent compliance requirements imposed by potential buyers, coupled with the unpreparedness of the Central Effluent Treatment Plant (CETP) at the Savar Tannery Industrial Estate, pose significant obstacles to fully harnessing Bangladesh’s labor export potential.

Addressing the negative perception of Bangladesh’s leather industry is crucial. Effective branding efforts are needed to establish a strong brand identity for Bangladeshi leather products in the global market, attracting buyers worldwide.

Future Trends and Opportunities

Opportunities include:

Expansive untapped markets both internationally and domestically.

A growing global demand for diversified, value-added products.

The potential for developing backward linkage businesses.

Opportunities for high-value addition, creating employment prospects.

The chance for local and foreign direct investment in the value-added leather products sector.

China’s declining competitiveness in this industry. They have begun to lose market share due to high labor costs.

Favorable government policies for leather exporters, including a DGeneralized System of Preferences (GSP) and cash incentives.

Increasing international and local demands for value-added leather products.

Interest from international fashion and sourcing companies in Bangladesh for leather goods.

The possibility of developing the entire supply chain, from raw leather processing to footwear and leather product production, domestically.