In the late 1990s, Bangladesh’s embrace of international markets and foreign direct investment (FDI) played a pivotal role in the rapid expansion of the Ready-Made Garments (RMG) sector. Today, RMG constitutes more than 83% of the country’s total export earnings. Of equal significance, during the late 1980s, the country’s banking system underwent extensive transformation. This involved the privatization of two previously financially troubled public banks, Pubali Bank and Uttara Bank, along with the issuance of licenses to private commercial banks. Another noteworthy structural reform introduced during this period was the adoption of back-to-back letters of credit (LCs), which significantly bolstered RMG exports. This innovation allowed banks to serve as intermediaries, managing two simultaneous LCs. This arrangement not only reassured buyers about the authenticity of their purchases but also provided sellers with a payment guarantee.

The financial system in Bangladesh can be broadly categorized into three distinct sectors, each characterized by its level of regulation:

Formal Sector: This sector encompasses all financial institutions that operate under regulatory oversight. This includes banks, non-bank financial institutions (FIs), insurance companies, and capital market intermediaries such as brokerage houses and merchant banks. Additionally, microfinance institutions (MFIs) also fall within the purview of the formal sector.

Semi-Formal Sector: In this sector, we find institutions that are subject to some form of regulation but do not fall directly under the authority of the central bank, insurance authority, securities and exchange commission, or any other established financial regulator. Specialized financial institutions like the House Building Finance Corporation (HBFC), Palli Karma Sahayak Foundation (PKSF), Samabay Bank, and Grameen Bank are prominent examples. Non-governmental organizations (NGOs) and discrete government programs also operate within this sector.

Informal Sector: The informal sector comprises private intermediaries that operate without any regulatory oversight. These entities function outside the boundaries of formal financial regulation.

Recent technological advancements have propelled Bangladesh’s financial sector forward. These include the automation of government securities trading through the Market Infrastructure (MI) Module, the implementation of the Automated Credit Information Bureau (CIB) for improved credit data management and risk mitigation, the introduction of the L/C Monitoring System for simplified Letter of Credit (L/C) administration, and the establishment of the Bangladesh Automated Clearing House (BACH) for seamless interbank settlements. Moreover, the expansion of mobile banking services to remote areas and the introduction of internet trading in both stock exchanges (DSE & CSE) exemplify the country’s commitment to modernizing its financial landscape, fostering efficiency, and promoting financial inclusion across diverse regions.

Key Factors Driving the Financial Services Industry

International Trade Growth (CAGR 8% in the last 4 years): Increasing trade activities drive demand for trade finance services, boosting banks’ roles in facilitating international transactions and contributing to sector growth.

Growing Remittance Inflow (CAGR 8.2% in the last 4 years): Growing remittances bolster financial institutions’ services and stimulate product demand, as banks play a vital role in facilitating remittance transfers.

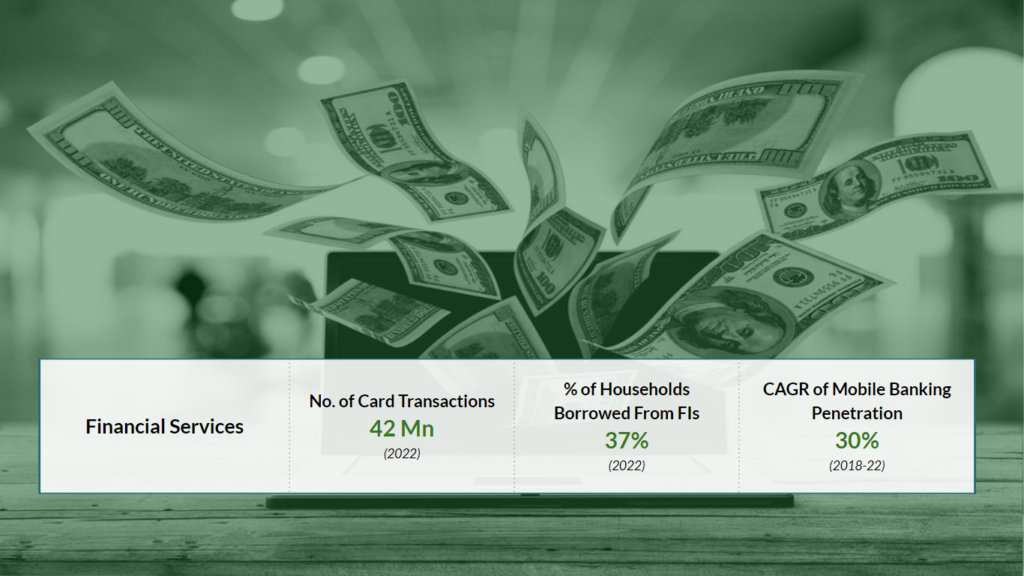

Rising number of Card Transactions (CAGR 22% in the last 4 years): The substantial increase in card transactions reflects a shift towards a cashless economy. This trend stimulates the demand for electronic payment services and drives growth in the financial sector.

Net FDI Inflow Growth (CAGR 12.8% in the last 4 years): The expanding foreign direct investment inflow creates opportunities for financial institutions to provide financing for projects, strengthening their role in the sector and contributing to its growth.

Mobile Banking Penetration (CAGR 30% in the last 4 years): The rapid growth in mobile banking penetration indicates increased accessibility to financial services, further expanding the reach of the financial sector and promoting financial inclusion.

Market Dynamics

According to a score of 346.2 on the Herfindahl-Hirschman Index (HHI), Bangladesh’s banking sector is highly competitive, leading to suboptimal decisions in terms of investments and loans. In comparison to the 43 private commercial banks (PCBs) among 61 scheduled banks, our neighboring country India has only 21 PCBs. Among the 35 publicly listed PCBs, BRAC Bank, Islami Bank, Dutch-Bangla Bank, and Eastern Bank are the top players in terms of market capitalization. There are 3 foreign-owned banks operational in Bangladesh, namely Standard Chartered Bank, HSBC, and Citibank.

During FY22, 739 licensed MFIs provided different types of financial services to 38.27 million

individuals where around 90 percent of the beneficiaries were women. The Microcredit Regulatory Authority( MRA) is in charge of regulating these institutions.

At present, Bangladesh has 35 life insurance companies, which include one foreign company and one public sector company. Additionally, there are 46 general (non-life) insurance companies, including one public sector company. The Insurance Development and Regulatory Authority (IDRA), founded in 2010, is responsible for overseeing and regulating the insurance sector in Bangladesh.

Bangladesh hosts 35 non-banking financial institutions among which 2 are entirely government-owned, 1 is a subsidiary of a state-owned commercial bank (SOCB), 19 are initiated through private domestic efforts, and 13 are established as foreign joint ventures. The primary sources of funds for these FIs include term deposits (with a minimum tenure of three months), credit facilities from banks and other FIs, call money, as well as bonds and securitization.

Challenges, Trends, and Opportunities

LightCastle Business Confidence Index (BCI) utilizes the Harmonized Expectation Indicator to take the geometric average between expectation and situation to provide a forward-looking quantitative output of the sentiment on a scale of –100 to +100, where a positive number indicates better expectations than current outcomes.

BCI Score

Financial Institutions

+0.82

Opportunities:

Green Banking: Bangladesh ranks as the third most active impact investing market in South Asia, signifying substantial potential for environmentally responsible investments.

Climate-Smart Investment: Bangladesh’s climate-smart investment potential is expected to soar to USD 172 billion by 2030. Investment opportunities span various sectors, including transport infrastructure, green buildings, renewable energy, agriculture, waste management, and urban water infrastructure financing.

Fintech Industry: The startup ecosystem within the fintech industry could achieve a valuation of USD 10 billion by 2025. This growth presents opportunities for the development and launch of innovative technologies, such as artificial intelligence (AI) and distributed ledger technology. Bangladesh Bank is inviting applications for digital banking licenses, having approved the Digital Bank guideline in June 2023, keeping provision for paid-up capital at Tk125 crore.

Insurance Sector: The insurance sector in Bangladesh offers diverse investment prospects, including bancassurance, microinsurance, green insurance, personal insurance protection, and agriculture. These opportunities collectively represent an investment potential of more than USD 600 million.

Microfinance Sector: The microfinance sector presents a significant investment opportunity of USD 1.4 billion. Key areas for investment include providing support to small and marginalized segments of society, including women and micro, small, and medium-sized enterprises (MSMEs).

Challenges:

Sovereign Credit Rating: Bangladesh’s long-term sovereign credit rating of BB- by Standard & Poor’s (S&P) reflects fundamental flaws. While the country can manage short-term financial needs, it would struggle to address significant long-term economic and financial challenges. A lower credit rating results in higher borrowing costs for Bangladesh, and any exposure of the banking sector could lead to severe consequences.

High Non-Performing Loans (NPL): As of 2022, the gross NPL to total loans ratio stood at 8.16%. This indicates a notable issue with non-performing loans within the banking sector, which can strain the financial stability of banks and reduce their capacity to lend and support economic growth.

Competitive Banking Sector: Bangladesh’s banking sector is highly competitive, which can sometimes lead to suboptimal decisions regarding investments and loans. Intense competition can create pressures to offer riskier loans or engage in less prudent financial practices, potentially increasing the overall risk in the sector.

Government Monetary Policy Interventions: The government frequently intervenes in the financial system through monetary policies, such as imposing interest rate caps. These interventions can compel financial institutions to make adjustments to their standard operating procedures, potentially impacting their profitability and ability to manage risks effectively