Bangladesh’s consumer durables industry is experiencing rapid growth, with significant potential for further expansion. Between 2016 and 2020, this industry achieved an impressive Compound Annual Growth Rate (CAGR) of approximately 14%, reaching a value of USD 2.4 billion in 2021. Given its cyclical nature, it has closely paralleled the country’s nominal GDP growth, and if it continues to grow at an annual rate of 17%, it is projected to reach the USD 10 billion milestone by 2030.

In the 1950s, several private companies were established in Bangladesh to produce radio sets, and as the country’s first television station came into existence in 1964, these assembly plants expanded to manufacture television sets as well. Prior to 1980, Bangladesh relied heavily on imports for domestic appliances and equipment. However, since the 1980s, the country has seen the emergence of assembly plants producing small home appliances like radios, televisions, and audio and video cassette players. The entry of Bangladesh into the World Trade Organization (WTO) free trade agreement in 1994 led to an increase in home appliance imports, making the market more competitive with the presence of foreign brands.

The consumer durables industry in Bangladesh comprises two segments: consumer appliances and consumer electronics. Consumer appliances can be further divided into Brown Goods and White Goods. Brown goods refer to consumer electronic items like televisions (TVs), computers etc, whereas, White goods refer to major appliances like washing machines and refrigerators. As of 2022, refrigerators had achieved the highest market penetration rate at 41.3%, while televisions followed closely with a penetration rate of 57.4% in the country. The consumer electronics sector is among Bangladesh’s fastest-growing industries, with many product categories reliant on imports, though local companies are also emerging. While consumer preference for foreign brands is on the rise due to their reputation for reliable services, only a few local companies can meet these demands. Despite the reliance on foreign brands, increased domestic production has led to growth, with companies like Walton even expanding their exports, thanks to government initiatives. Currently, domestic firms like Fair Group, Butterfly Group, Electra, Rangs Group, Electro Mart, and Transcom Group engage in the production and assembly of Electronics Home Appliances in partnership with international brands such as Samsung, Whirlpool, LG, Sony, Gree, Konka, and Sharp.

At present, the BCI score stands at -11.85. This is mainly influenced by the negativity attributed to the current economic downturn and the high import costs. Nevertheless, there is a ray of hope for maintaining a stable performance in the present, along with chances to enhance operational efficiency at the current performance level.

Key Factors Driving the Consumer Durables Industry

Growing GDP per capita and growing buying power of the populace: According to data from the World Bank, GDP per capita increased to USD 2688.3 in 2022 from USD 2457.9 in 2021. Consumer gadgets have been in greater demand over time as people’s purchasing power has grown.

Greater coverage of power: Bangladesh has made enormous strides toward increasing access to electricity, and as of 2023, 100% of the population will be covered by electricity. By 2030, the peak demand is anticipated to increase by an average of 12.2% each year to 35,000 MW. With this rise in demand, we anticipate that the consumer durables sector will continue to grow at its present rate for at least the next ten years.

The growing impact of global warming has resulted in an increased need for specific items such as air conditioners and refrigerators.

The expanding middle-class (MAC) population and the trend toward smaller nuclear families are expected to have a significant impact. By 2025, the MAC population is projected to reach approximately 34 million, with around 63 cities having at least 100,000 MAC residents. As nuclear families continue to rise, the desire for convenience is expected to surge, resulting in greater demand for consumer electronics.

Shifting consumer behavior is redefining the status of consumer electronics. Once considered exclusive luxury items, these products are now viewed as essential household necessities due to the urbanization of Bangladesh.

Government incentives and policies are contributing to the sector’s growth. Initiatives such as reduced advance taxes on raw materials have reduced production costs, making these products more affordable.

The availability of increasing financial schemes, facilitated by companies offering mobile financial services (MFS), is driving up demand. Companies like Singer and Walton provide hire purchase plans, enabling consumers to make installment payments and allowing those with lower disposable incomes to access these products. Expanding financial schemes through MFS also extends the opportunity to the unbanked population.

The proliferation of digital channels, e-commerce platforms, and social commerce (F-commerce) platforms has significantly boosted brand awareness and expanded reach, resulting in heightened demand for these products.

Export Potential

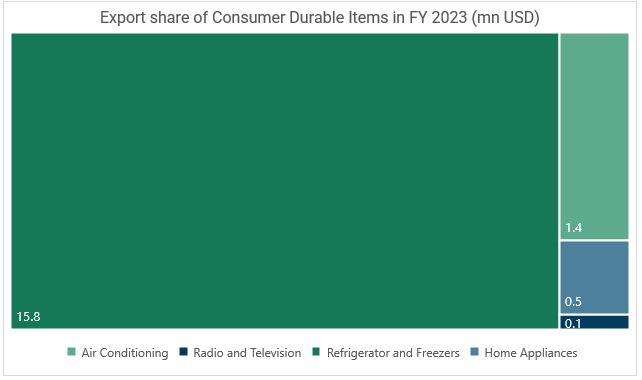

According to data from the Export Promotion Bureau, Bangladesh generated $115.30 million in revenue from the sale of electrical and electronic products in international markets during the first 11 months of the 2022-23 fiscal year, which marks a significant increase from the $77.86 million earned during the same period in the preceding year. These domestically produced goods are finding their way to over 40 countries across the globe. The exportable items comprise compressors and their components, refrigerators, televisions, air conditioners, home appliances, mobile phones, and laptops, among others. This industry has played a prominent role in promoting the “Made in Bangladesh” slogan on the international stage, and the global response has been exceedingly positive.

Market Dynamics

As reported by Marketing Watch Bangladesh, televisions account for 30.03% of the total electronics product sales in Bangladesh. Furthermore, the data indicates that local manufacturers dominate 52% of the country’s television market, with Walton leading the pack with a market share exceeding 25%. Additionally, Singer holds a 9% share, Minister holds 4%, Vision holds 3%, and Jamuna holds 2%.

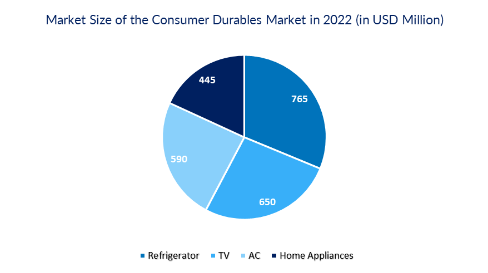

In the realm of home appliances, refrigerators play a significant role. The estimated market size for refrigerators in Bangladesh in 2021 reached $765 million. In the same year, the air conditioner market in Bangladesh was valued at $590 million. Similar to the refrigerator industry in Bangladesh, approximately 65% of the local demand for air conditioners is met locally, while the remaining 35% is fulfilled through imports.

Government Support & Policy Incentives

The government is consistently offering both fiscal and non-fiscal incentives to promote domestic manufacturing, such as corporate tax breaks and reduced import duties on raw materials. Some of these incentives include:

Starting from July 2021, companies involved in the production of home and kitchen appliances can enjoy a 10-year tax exemption.

There is also a Value Added Tax (VAT) exemption for the manufacturing of washing machines and kitchen appliances.

The advance tax for importing raw materials for local production has been reduced from 4% to 3%.

Manufacturers of home and kitchen appliances can continue to benefit from tax exemptions until mid-2031, provided that they achieve a local value addition of at least 30%.

Additionally, as part of Vision 2041, the government aims to ensure equitable distribution of benefits for future growth, especially in the electronics sector, through rapid advancements.

Investment Challenges and Mitigation Strategies

Among the difficulties the sector is now facing are:

Imports of essential raw materials, spare components, and completed goods are crucial to the industry. Since there are no suitable supporting industries, components must mostly be imported. There is no backward linkage industry for local producers in the home appliance sector.

Despite reaching 100% electrification, there is still an intermittent scarcity of electricity and energy, which disrupts manufacturing.

There is an uncontrolled Grey market where mobile gadgets are mostly sold; according to one responder, 53% of their mobile brand is sold there.

Company predictions and long-term company planning are hampered by the continuously shifting industrial provisions in fiscal and monetary policies.

Future Trends and Opportunities

Smaller companies are increasingly teaming up with foreign technology partners to compensate for their technological limitations, and they find Semi Knocked Down (SKD) manufacturing preferable because it requires a comparatively lower investment. Over time, these companies aim to delve deeper into the value chain through Completely Knocked Down (CKD) manufacturing.

The utilization of a digital customer engagement model offers significant potential for brands to access customer information. Developing effective data control and data monetization strategies will be pivotal for the consumer electronics industry in the forthcoming years.

Additionally, as China shifts its focus towards high-tech and heavy industries, medium and low-tech industries are relocating to South Asian countries. China is no longer able to take advantage of low-cost labor due to the rising skill level of its workforce. Conversely, because Bangladesh boasts lower labor costs than other countries and continually advances its skills in the IT and light engineering sectors, it is well-positioned to seize this opportunity in the future and become a hub for manufacturing essential consumer electronics.