Bangladesh presents a promising market for the expansion of the automobile industry, driven by rapid motorization and rising consumer demand. As of 2024, the country is currently registering approximately 500,000 additional vehicles annually, reflecting strong growth in mobility demand and economic activity.

Motorization growth is particularly evident in motorcycles, where registrations increased fivefold from 0.67 million in 2010 to 4.2 million in 2023, highlighting strong consumer-driven expansion.

At a macro level, this trend is supported by the World Bank, which notes that Bangladesh’s registered vehicle fleet expanded dramatically to over 6 million vehicles by 2024, driven by urbanization, economic growth, and rising transport demand.

Despite this rapid growth, Bangladesh remains a low-penetration market, with only 6 vehicles per 1,000 population, indicating significant untapped potential for future expansion.

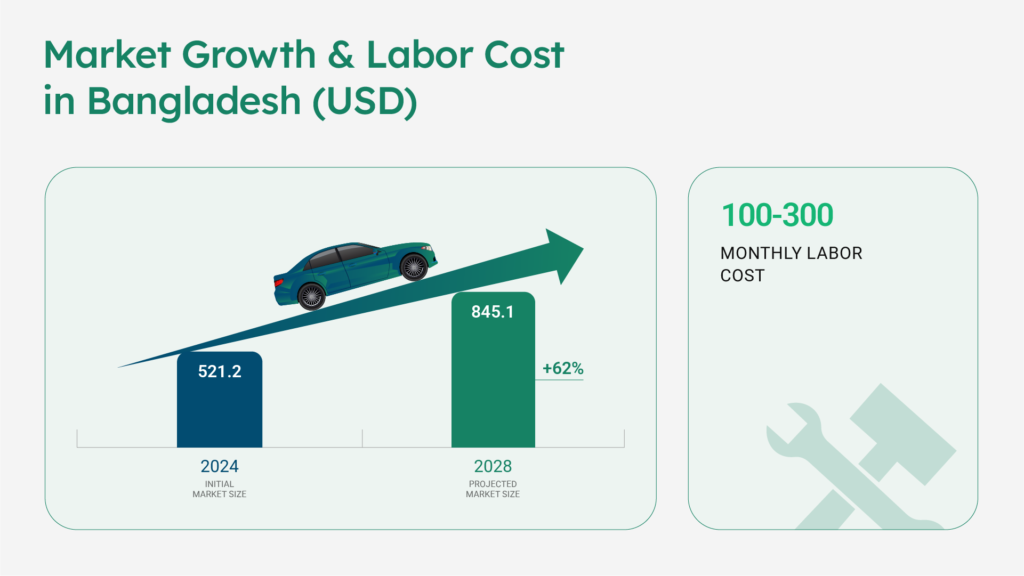

From a market perspective, the passenger car segment generated approximately USD 521.2 million in 2024 and is projected to grow at a CAGR of 12.84% (2024–2028), reaching around USD 845.1 million by 2028, demonstrating strong medium-term demand potential.

On the supply side, the sector remains largely assembly-based, with CKD/SKD operations dominating. Global and local players, including Hyundai, Proton, Honda, Yamaha, Bajaj, and Walton, operate assembly facilities, while domestic firms are gradually increasing value addition through partial manufacturing. Additionally, Bangladesh offers a strong cost advantage, with automobile sector labor costs ranging between USD 100–300 per month, significantly lower than regional competitors, enhancing its attractiveness for manufacturing investment.

However, structural challenges remain. According to the World Bank, Bangladesh’s vehicle ecosystem is characterized by:

- Aging vehicle fleet (especially buses and trucks)

- High reliance on fossil fuels

- Weak inspection and emission control systems

These factors highlight the need for modernization and regulatory strengthening. Short-term sector performance is also affected by macroeconomic conditions.

The consumer electronics/automobile-adjacent segment recorded a BCI score of -6.08 in 2024-45, reflecting weak demand due to inflation, high import costs, and reduced consumer purchasing power.

This aligns with broader economic challenges, including high interest rates, currency depreciation, and constrained import conditions, impacting CKD/SKD assembly operations.

Looking ahead, the sector is gradually shifting toward higher-value manufacturing and future mobility, particularly:

- Electric vehicles (EVs) and hybrid technology

- Auto parts and component manufacturing

- Specialized logistics vehicles

These areas are identified as key foreign investment opportunities.

Bangladesh’s passenger vehicle market continues to be dominated by reconditioned vehicles, which remain the largest segment of imports and sales. In 2024, over 80% of the nearly 24,000 passenger vehicles sold were Japanese reconditioned cars, indicating that the market remains strongly price-sensitive and dependent on imported used vehicles. By FY2025, the structure remained similar, with reconditioned vehicles accounting for around 75% of total car imports, while brand-new vehicles made up the remaining 25%. This confirms that despite growing interest in local assembly and brand-new models, reconditioned cars still hold the dominant market position in Bangladesh.

In the brand-new segment, locally assembled vehicles are gaining traction, with Hyundai capturing one-third of the new-car market and ranking third overall, behind Toyota and Honda.

Segment-wise, cars up to 1600cc dominate (~70%), while SUVs and hybrids are the fastest-growing categories, with hybrids accounting for nearly half of imported cars. Moreover, the Bangladesh agricultural tractor market is forecast to grow at a 9% CAGR through 2025–2031, driven by government mechanization programs, rising labor costs, and adoption of modern farming practices.

Despite global trends, EV penetration remains negligible, with only ~400 EVs registered out of over 6 million vehicles as of 2024. Additionally, Bangladesh hosts several local private automobile assembly companies, including IFAD Autos Ltd, Aftab Automobiles, Fair Technology Limited, Bangladesh Auto Industries Limited, Bangladesh Machine Tools Factory, Bangla Cars, Niloy-Hero Motors, PHP Automobiles, Pragoti Industries Limited, Runner Automobiles, and Uttara Motors Limited.

As of 2024-2025, the Government of Bangladesh provides the following support and policy incentives for the automobile and transport sector:

Several investment hurdles include:

The automotive industry in Bangladesh offers significant investment opportunities, driven by rising demand for both passenger and commercial vehicles, favourable economic policies, and attractive fiscal incentives. Electric vehicles (EVs) represent a key long-term opportunity, supported by early investments (e.g., a BDT 1,440 crore EV component plant by Bangladesh Auto Industries Limited) and growing private-sector interest, though infrastructure gaps remain.

According to BIDA, there is also strong potential in auto parts and component manufacturing, driven by low labour costs and expanding assembly activities. Overall, the sector is expected to evolve from a reconditioned-import-dominated market to a more diversified ecosystem, including locally assembled vehicles, hybrids, and eventually EVs, driven the potential the market currently poses and the global shift towards renewable-fueled transportation.

Gain perspectives of the emerging sectors of Bangladesh

InsightsContact us for a comprehensive understanding of the investment landscape in Bangladesh