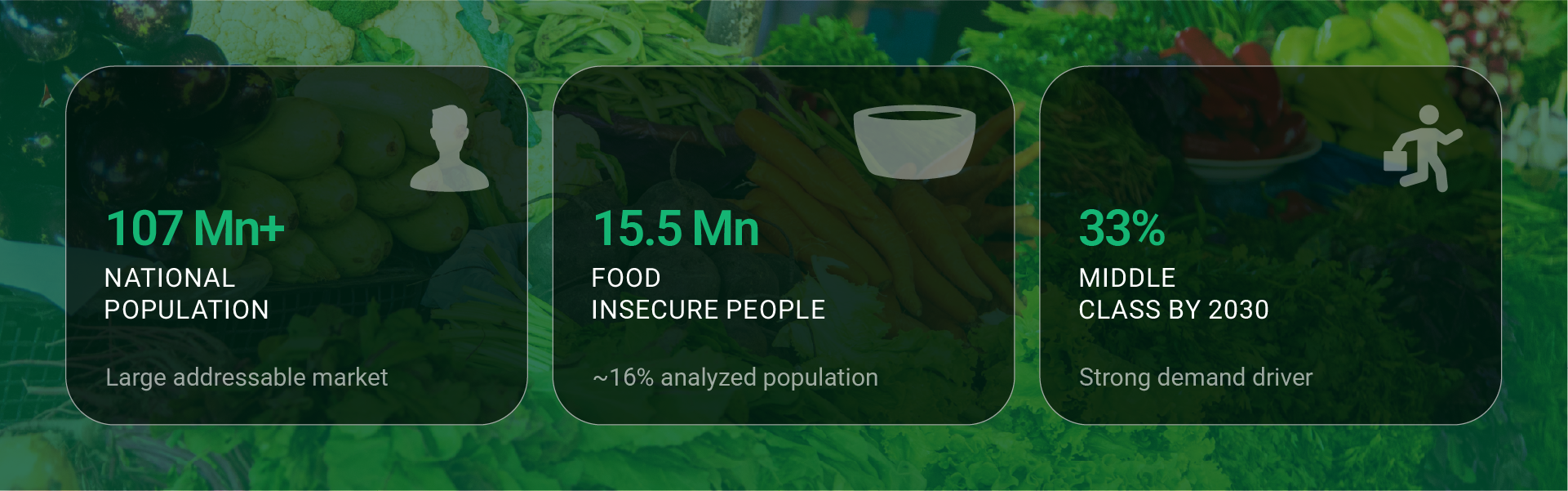

Bangladesh’s food and nutrition sector is a critical pillar of the national economy, ensuring food security for a population of more than 170 million while supporting employment across agriculture, aquaculture, food processing, and distribution value chains. Over the past decades, the country has achieved significant gains in food production, particularly in rice, fish, poultry, and livestock, which together form the backbone of the domestic food system. Despite strong production growth, food security remains an important policy priority. As of 2025, approximately 15.5 million people, around 16% of the analyzed population, are experiencing high levels of acute food insecurity, including 361,000 people in emergency, reflecting the impact of climate variability, inflationary pressures, and livelihood vulnerabilities. This fragility is exacerbated by the lingering effects of 2024 climatic shocks, such as Cyclone Remal, which caused widespread flooding and asset depletion Nutritional outcomes for children are a severe concern, with 1.6 million children aged 6-59 months suffering or expected to suffer from acute malnutrition between January and December 2025.

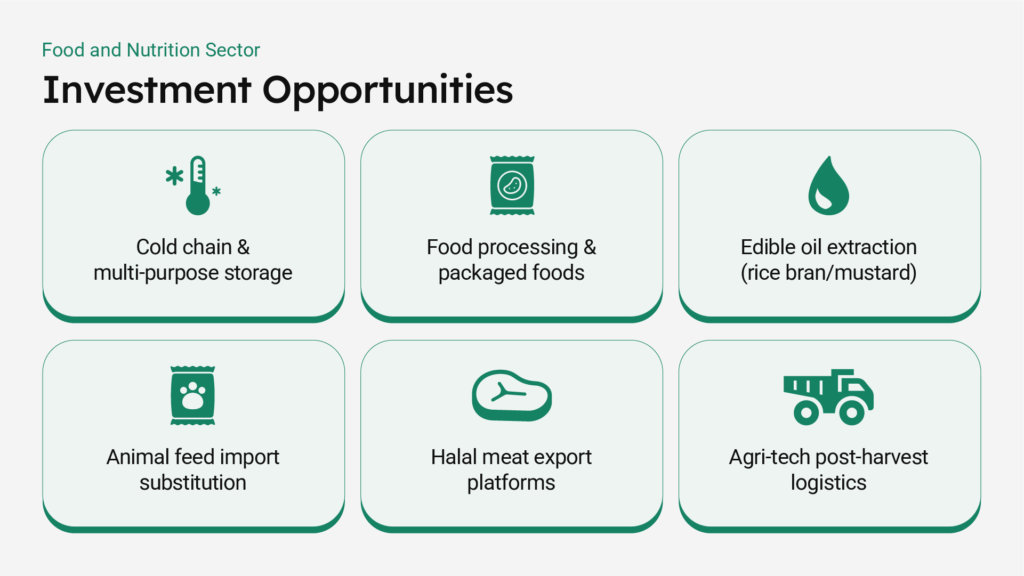

In response to these interlinked food security challenges, coordinated action across government, development partners, and the private sector has become imperative. Strengthening food security has been one of the core agendas for the country. To mitigate the current risks and barriers, the government and development partners are investing in food system resilience through initiatives such as modern grain storage infrastructure, nutrition-sensitive agriculture, and improved food distribution systems to enhance national food security and reduce supply disruptions.

Driven by the factors, actual daily food intake shifted significantly over the years. Per capita rice consumption declined while intake of fruits, vegetables, and meat rose due to rising incomes, urbanization, and changing dietary preferences toward more diverse and protein-rich foods. However, demand fundamentals remain strong due to Bangladesh’s expanding population and a growing middle class. Rising household consumption is expected to drive demand for packaged and processed food products, particularly as the middle and working class is projected to reach 33% of the population by 2030, supporting expansion in the food processing industry. Cost pressures remain a major market driver. On the supply side, prices for livestock feed have increased significantly due to global commodity fluctuations. For example, the cost of cattle feed, particularly wheat bran, rose by approximately BDT 7–10 per kilogram in FY2024–2025, increasing production costs across aqua, poultry and livestock operations. Additionally, Bangladesh’s reliance on imported feed inputs has increased, with soybean imports for poultry feed rising from around 15% before 2022 to nearly 40% following the Russia–Ukraine conflict. On the production side, seed, fertilizer, and irrigation technologies have played a major role in raising Bangladesh’s rice production over time. Continued focus on improved seed adoption and proper fertilizer application can further support farm productivity and strengthen the agri-food supply base.

Beyond the domestic market, Bangladesh exports fresh products and packaged food items primarily to destinations like the US, Europe, and the Gulf nations, where the migrant network of the country is strong. The bulk of the export revenue comes from aquaculture products. To diversify this export basket from dependence on aqua products, the government and private sector are working to facilitate the introduction of more efficient production technologies in the sector, establish a robust post-harvest storage infrastructure, and improve food security monitoring standards to unlock the export potential of the sector. The government has launched the Khamari App, a BARC-developed geospatial tool providing farmers with crop-specific fertilizer and market guidance, already deployed across multiple districts , while finalizing the Agriculture Future Outlook Plan 2025 to scale production technologies nationally.

Despite persistent economic pressures, private sector business sentiment remains resiliently positive, led by an increased Business Confidence Index (BCI) score for poultry and livestock, signaling cautious optimism for investment and market expansion as food inflation stabilizes and domestic demand continues to grow.

LightCastle Business Confidence Index (BCI) uses the Harmonized Expectation Indicator to compute the geometric average of expectations and current outcomes, providing a forward-looking quantitative measure of sentiment on a scale of –100 to +100, where a positive number indicates better expectations than current outcomes.

| Sector | BCI Score (2024-2025) |

| Poultry & Livestock | +14.9 |

| Aquaculture | +8.29 |

| FMCG | +7.49 |

The positive BCI scores across poultry and livestock, aquaculture, and FMCG indicate cautious optimism among businesses, with expectations for future performance remaining stronger than current market conditions. However, despite this improving sentiment, each sector continues to face structural and operational challenges that must be addressed to unlock sustained growth.

Challenges:

Opportunities:

Gain perspectives of the emerging sectors of Bangladesh

InsightsContact us for a comprehensive understanding of the investment landscape in Bangladesh