Figure 1 About Leather and Footwear Sector in Bangladesh

The leather and footwear industry in Bangladesh is an emerging export-oriented sector with strong potential to diversify the country’s export basket beyond ready-made garments. The sector is gaining importance as a high-potential industry under national diversification strategies, supported by growing production capacity and evolving global demand trends. From a business sentiment perspective, the sector reflects a positive outlook with a Business Confidence Index score of +9.16 in 2024-2025, indicating higher confidence among industry stakeholders despite existing challenges.

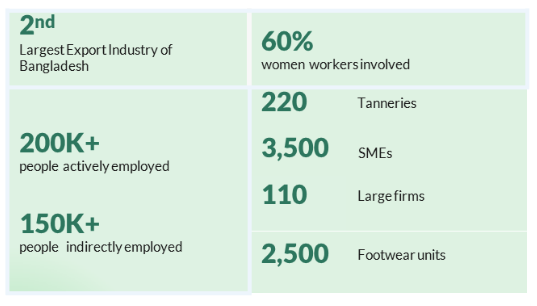

Bangladesh ranks as the 8th largest footwear producer globally, with production significantly exceeding domestic consumption, resulting in a surplus of around 68 million pairs. These surplus supports export expansion, with 20.1% of total production directed toward international markets, outperforming regional peers such as India and Pakistan. Bangladesh holds approximately 3% of the global leather and leather products market and represents around 10% of the worldwide leather market by volume.

The industry encompasses multiple segments, including tannery operations, finished leather, leather goods, and footwear, producing a wide range of items such as shoes, bags, belts, and accessories. Among these, non-leather footwear (rubber, plastic, and textile) dominates export volume, reflecting global consumer shifts toward affordability and sustainability. However, leather footwear continues to command higher global prices, indicating significant untapped potential for Bangladesh to move into higher-value segments.

Bangladesh’s footwear exports are primarily concentrated in traditional markets such as the United States and European countries including Germany, France, and the Netherlands, while also expanding into emerging markets like India, China, and Japan. The country benefits from duty-free access to EU markets under the EBA initiative, making market diversification and trade agreements increasingly important.

Despite strong fundamentals, the sector faces structural constraints. The industry remains largely positioned in the mid-value segment, with limited progress in value addition, as reflected in Bangladesh’s low Economic Complexity Index ranking (109th globally). Additionally, environmental compliance challenges, particularly the lack of adequate Central Effluent Treatment Plant (CETP) for different market players, continue to hinder access to premium global markets and affect sustainability positioning.

Overall, Bangladesh’s leather and footwear sector stands at a critical transition point, where its future growth will depend on enhancing value addition, improving compliance standards, and expanding into higher-value global markets. With continued policy support, investment, and strategic positioning, the sector has the potential to become a major contributor to Bangladesh’s export-led industrial growth.

Key Factors Driving the Livestock & Fisheries Industry

Strong production capacity and surplus output: Bangladesh has built a robust manufacturing base with large-scale production capacity, producing significantly more footwear than domestic demand. In 2023, the sector generated a surplus of around 68 million pairs, enabling expansion into export markets.

Growing export orientation and market expansion: Around 20.1% of total production is exported, indicating growing integration into global markets and highlighting strong potential for further export expansion.

Alignment with global demand trends: Global consumers are shifting toward non-leather footwear (rubber, plastic, and textile) due to affordability and sustainability concerns. Bangladesh is already aligned with this trend, with a significant share of exports concentrated in these segments.

Access to major international markets: Bangladesh benefits from strong trade relationships with key markets such as the United States and the European Union, supported by preferential access (e.g., EBA), which enhances export competitiveness.

Emerging opportunities in new markets:The country is expanding into emerging markets such as India, China, and Japan, driven by rising demand and increasing purchasing power in these regions, helping diversify export destinations.

Cost competitiveness with mid-tier positioning: Bangladesh maintains a competitive advantage in the mid-range footwear segment, offering relatively affordable products while maintaining quality. However, there remains a significant opportunity to move into higher-value segments.

Policy focus on export diversification: With Bangladesh aiming to reduce dependence on the RMG sector, the footwear industry has been identified as a high-potential sector for diversification and FDI attraction, supporting long-term growth.

Export Potential

In FY 2024–25, earnings from leather and leather products grew by 10.19% year-on-year to reach USD 1.14 billion. Within this, leather footwear remained the largest export segment, contributing 23.54% to USD 672 million, followed by leather products at USD 353 million and finished leather at USD 143 million. Encouragingly, finished leather exports recorded a strong growth of 15.49%, while non-leather footwear exports expanded by 8% to reach USD 417 million, reflecting a gradual shift toward value-added and diversified product segments.

A significant share of Bangladesh’s leather, leather products, and footwear output is export-oriented, with international markets serving as the primary destination for growth in the sector. The industry exports a wide range of products, including crust leather, finished leather, leather goods, and footwear. Key export destinations include the European Union, the United States, Japan, China, and other developed markets, benefiting from preferential market access in several of these regions.

Strengthening domestic processing capabilities and transitioning toward higher-value finished products will be critical for enhancing export earnings and reinforcing Bangladesh’s position in global leather markets.

Market Dynamics

Bangladesh’s footwear sector is at an important turning point, shaped by shifting global demand patterns. As of 2025, Asia accounts for 54.7% of total consumption, while demand is moving away from leather toward rubber, plastic, and textile-based footwear. Bangladesh is already aligned with this trend, with around 94% of its footwear exports being non-leather products, positioning the country well within evolving global preferences.

At the foundation of this sector lies the leather value chain, which begins with domestic sourcing of raw hides and skins (RHS), largely supplied by small-scale livestock farming, with 97% of animals raised on small farms. A significant portion of supply is concentrated during Eid-ul-Azha, creating seasonal fluctuations. However, inefficiencies in procurement, driven by multiple intermediaries and the absence of standardized grading, continue to increase costs and distort pricing.

The next stage involves transformation through tanneries, where RHS is processed into wet blue, crust, and finished leather, progressively adding value. The shift from crust to finished leather is particularly critical, requiring advanced technology and skilled labor. At the same time, environmental compliance remains a persistent challenge, especially due to the partial functionality of the CETP at Savar, which limits full alignment with international standards.

Building on this foundation, the industry is gradually moving toward higher-value manufacturing, particularly in footwear. The sector has demonstrated strong recovery in FY 2024–25, supported by rising global demand, increasing export orientation, and policy incentives. As a result, Bangladesh is becoming more integrated into global value chains, with growing potential for further export expansion.

Despite this progress, the sector remains largely positioned in the mid-range segment, with an average export price of USD 14.97 per pair, indicating limited penetration into premium markets. The country’s Economic Complexity Index ranking of 109th out of 132 further highlights the need for greater value addition and diversification into higher-end products.

Looking ahead, these challenges may intensify as Bangladesh approaches LDC graduation in 2026, which could reduce preferential access to key markets such as the EU. At the same time, sustainability and environmental compliance, particularly addressing gaps in CETP functionality, are becoming increasingly critical, not just as competitive advantages but as essential requirements for continued market access.

Challenges, Trends and Opportunities

Challenges:

Reduced Corporate Income Tax (CIT) for 5–10 years based on location applicable until 30 June 2030.

50% tax exemption on income from exports applicable until 30 June 2028.

No VAT on export goods applicable from 02 June 2025.

Import duty-free capital machinery applicable from June 2, 2025.

10% export subsidy on leather goods applicable until 31 December 2025.

Leather and Leather Products Development Policy 2019 have comprehensive incentives to boost exports.

Investment Challenges

Some of the challenges include:

Implementation gaps within the existing policy framework, including a lack of a long-term strategy for Common Facility Centers (CFCs), SME cluster development, and the promotion of Bangladesh leather products.

Insufficient development of backward linkage industries for chemicals and accessories, along with issues related to the subpar quality of products.

The stringent compliance requirements imposed by potential buyers, coupled with the underperformance of the Central Effluent Treatment Plant (CETP) at the Savar Tannery Industrial Estate, pose significant obstacles to fully harnessing Bangladesh’s labor export potential.

Overcoming perception barriers related to environmental compliance and product quality of Bangladesh’s leather industry is crucial. Sustained investment in compliance, traceability, and branding is needed to shift buyer perception and strengthen trust in Bangladeshi leather and footwear products, particularly in premium markets.

Future Trends and Opportunities

Opportunities include:

Expansive untapped markets both internationally and domestically.

The potential for developing backward linkage businesses.

Opportunities for high-value addition, creating employment prospects.

The chance for local and foreign direct investment in the value-added leather products sector.

Shifting global manufacturing dynamics, as rising labor costs in major producing economies redirect sourcing toward cost-competitive destinations.

Favorable government policies for leather exporters, including a Generalized System of Preferences (GSP) and cash incentives.

Increasing international and local demands for value-added leather products.

Interest from international fashion and sourcing companies in Bangladesh for leather goods.

The strategic opportunity of developing the entire supply chain, from raw leather processing to footwear and leather product production, domestically with investment in CETP, upskilling, and value-addition context