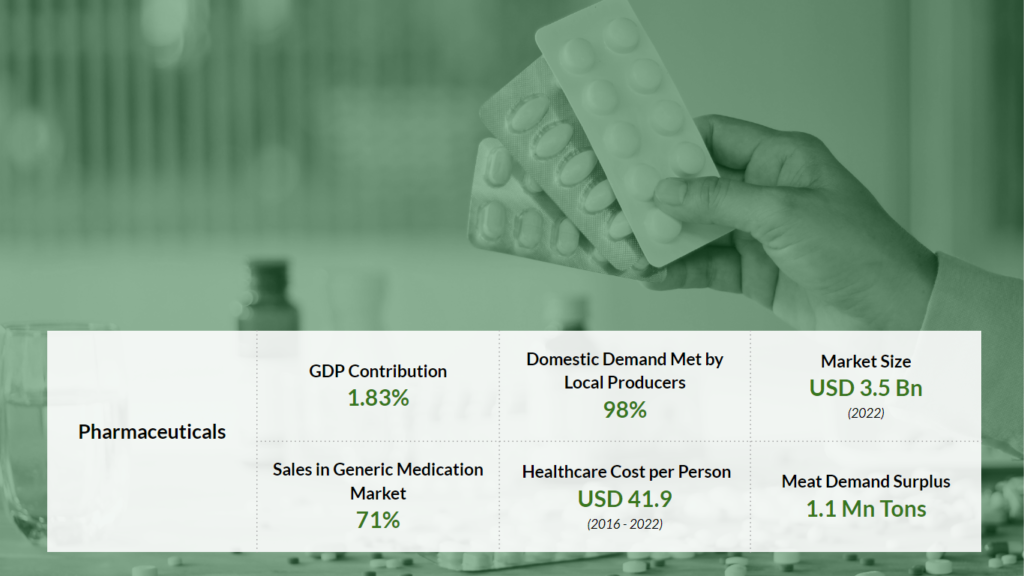

Over the last decade, Bangladesh’s pharmaceutical industry has grown substantially, contributing 1.83% to the country’s GDP. The industry’s notable expansion didn’t commence until the 1980s when Bangladesh was granted patent exemption in the pharmaceutical sector, following its designation as a developing nation. Currently, domestic pharmaceutical manufacturers can fulfill 98% of the country’s total demand for medicines. The market size of the sector has reached approximately USD 3.5 billion (as of 2022, up from USD 3 billion in 2019), and it is projected to exceed $6 billion by 2025, representing a remarkable 114% absolute growth rate since 2019. Furthermore, the industry has sustained an impressive Compound Annual Growth Rate (CAGR) of 15.6% over the past five years.

At present, Bangladesh produces more than 450 generic drugs under 5,300 well-known brands and meets 4% of the nation’s requirement for anti-cancer medications. According to the Director General of Drug Administration (DGDA), the pharmaceutical sector encompasses 3,657 registered generic allopathic drugs, 2,400 registered homeopathic drugs, 6,389 registered unani drugs, and 4,025 registered ayurvedic drugs. Approximately 71% of pharmaceutical sales are attributed to the generic medication market. There are over 150 enterprises engaged in formulation production, with 30 of them involved in exports.

Additionally, around 40 companies are involved in the manufacturing of bulk drugs, and there are over 40 manufacturing units producing active pharmaceutical ingredients (APIs).

Due to LDC status, patented products imported into Bangladesh are priced significantly lower than in many other countries, allowing for their re-export to developed nations. Bangladesh also exports Active Pharmaceutical Ingredients (APIs). Furthermore, as per the Bangladesh Bureau of Statistics (BBS), the individual healthcare expenditure in Bangladesh surged threefold in the preceding decade, soaring from $15.8 to $41.9 per person. During this period, the count of private healthcare establishments escalated from 3,536 in 2000 to 16,979 in 2021. These private healthcare facilities are distributed as follows: private diagnostic centers constitute 60.61%, private hospitals make up 26.22%, private medical clinics represent 8.23%, and private dental clinics account for 4.99% of the total.

Furthermore, the Active Pharmaceutical Ingredient, commonly known as API, serves as the fundamental component of every completed drug product. In the case of small molecules, APIs constitute 30% of the overall drug expenses, and this percentage can rise to as much as 55% for generic products. Presently, Bangladesh fulfills 98% of the demand for finished pharmaceutical products within the country. However, despite achieving near self-sufficiency in the production of finished drugs, over 90% of the required APIs and raw materials must be imported. The majority of Active Pharmaceutical Ingredients (APIs) are procured from countries such as India, China, Italy, and Germany. Specifically, around 40% of the raw materials originate from China, while approximately 30% are sourced from India.

This heavy reliance on imported raw materials exposes the pharmaceutical industry to potential disruptions in the supply chain and fluctuations in prices. Consequently, the lack of a robust backward linkage has emerged as a significant challenge for our promising pharmaceutical sector.

With a remarkable BCI score of +33.18 at present, which reflects an exceptional positive rating, the pharmaceutical sector in Bangladesh has experienced a noteworthy period of growth. Although the industry may encounter challenges related to the potential loss of LDC benefits, it still holds substantial export potential for generic drugs.

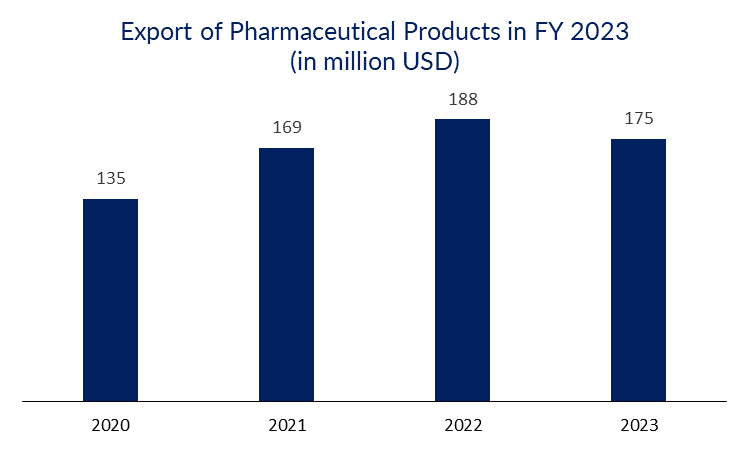

In the fiscal year 2022, exports amounting to $188.8 million were shipped to 157 countries across Asia, Africa, North America, South America, and Europe. Notably, 90% of the medications supplied to the United States are sourced from Beximco Pharmaceuticals. More than 20 pharmaceutical companies from Bangladesh, including Incepta, Beacon, Square, Popular, Eskayef, Beximco, Opsonin, ACI, Renata, and Ziska, have reportedly exported COVID medications, with a particular increase in the export of antiviral drugs such as Remdesivir and Favipiravir.

Presently, Bangladesh’s pharmaceutical sector is striving to capture 10% of the global market. Recognition and authorization have been granted by international bodies such as the World Health Organization (WHO), the World Trade Organization (WTO), and the World Intellectual Property Organization (WIPO) to six national organizations.

According to data from the Bangladesh Association of Pharmaceutical Industries (BAPI), over the past two years (2019 and 2020), more than 1,200 pharmaceutical products have been registered for export in Bangladesh. It is anticipated that the export potential will grow significantly, increasing from approximately $169 million in the fiscal year 2020-21 to over $450 million USD by the year 2025. Furthermore, as Bangladesh is trying to enhance API production this will further diversify exports and open up more opportunities and markets.

The domestic market is made up of more than 60% of the top ten firms in this industry and more than 80% of the top twenty. Square, Incepta, Beximco, Renata, Opsonin, Healthcare Pharma, Eskayef, Beacon, and ACI are a few of the leading market participants. 32 of the country’s pharmaceutical firms are listed on the DSE, including the top five market players Square Pharmaceuticals, Beximco, Renata, Acme, ACI, and Ibn Sina. Furthermore, currently, 15 Bangladeshi companies, including Square Pharma, Beximco Pharma, Active Fine, ACI Limited, Globe Pharma, Gonoshasthaya Pharma, Opsonin Pharma, Drug International, and Eskayef, collectively manufacture approximately 40 Active Pharmaceutical Ingredients (APIs). Gonoshasthaya Pharmaceuticals Limited (GPL) stands out as the leading contributor, accounting for approximately 60% of locally manufactured APIs.

As of 2021, the pharmaceutical and chemicals sector constituted a mere 1.94% of the total foreign direct investment, with the United Kingdom contributing 40.6%, India 7.1%, and the Netherlands 5.7% to this sector’s foreign investments. The pharmaceutical industry in Bangladesh is currently grappling with a deficiency in research initiatives undertaken by domestic pharmaceutical companies. Consequently, the local pharmaceutical sector is facing challenges in terms of innovation and lacks a strong focus on research and development.

To enhance competitiveness, a reduction in the corporate tax rate is needed as it currently exceeds that of competing nations. To mitigate the effects of LDC graduation, the government should continue supporting the export sector through tax incentives, while also implementing automation measures to streamline tax collection processes.

The European Market is encountering significant difficulties due to the recent surge in the manufacturing expenses of generic drugs. Additionally, a number of major drugs are projected to lose their patents in the EU markets in 2022, creating opportunities for generic drug producers. In the United States, patent expirations for certain drugs are also anticipated in the years 2023-2024. Bangladesh is swiftly gaining recognition as a global supplier of cost-effective, high-quality generic medications, and the nation can take advantage of this trend. Furthermore, Increased FTA with Cambodia, Japan, Brazil, and other countries will lead to increased access to these markets even after LDC graduation. Also, enhancing the capacity for API production will substantially reduce Bangladesh’s over-reliance on imports and augment its competitive edge in the global market.

Gain perspectives of the emerging sectors of Bangladesh

InsightsContact us for a comprehensive understanding of the investment landscape in Bangladesh